Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Should I Wait for Mortgage Rates To Come Down Before I Move?

If you’ve got a move on your mind, you may be wondering whether you should wait to sell until mortgage rates come down before you spring into action. Here’s some information that could help answer that question for you.

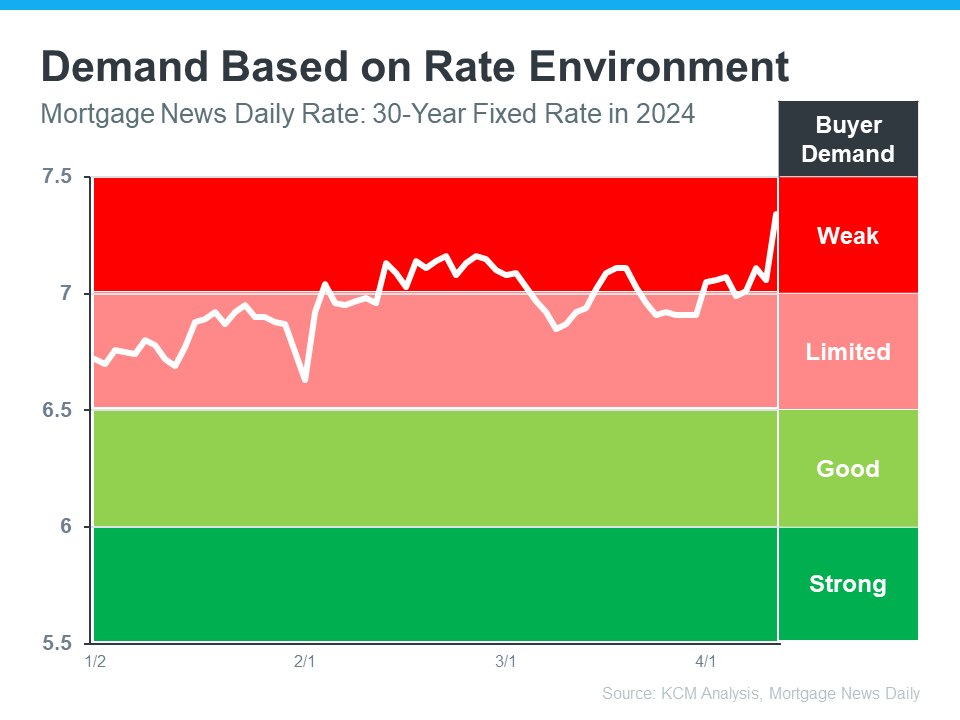

In the housing market, there’s a longstanding relationship between mortgage rates and buyer demand. Typically, the higher rates are, you’ll see lower buyer demand. That’s because some people who want to move will be hesitant to take on a higher mortgage rate for their next home. So, they decide to wait it out and put their plans on hold.

But when rates start to come down, things change. It goes from limited or weak demand to good or strong demand. That’s because a big portion of the buyers who sat on the sidelines when rates were higher are going to jump back in and make their moves happen. The graph below helps give you a visual of how this relationship works and where we are today:

As Lisa Sturtevant, Chief Economist for Bright MLS, explains:

“The higher rates we’re seeing now [are likely] going to lead more prospective buyers to sit out the market and wait for rates to come down.”

Why You Might Not Want To Wait

If you’re asking yourself: what does this mean for my move? Here’s the golden nugget. According to experts, mortgage rates are still projected to come down this year, just a bit later than they originally thought.

When rates come down, more people are going to get back into the market. And that means you’ll have a lot more competition from other buyers when you go to purchase your next home. That may make your move more stressful if you wait because greater demand could lead to an increase in multiple offer scenarios and prices rising faster.

But if you’re ready and able to sell now, it may be worth it to get ahead of that. You have the chance to move before the competition increases.

Bottom Line

If you’re thinking about whether you should wait for rates to come down before you move, don’t forget to factor in buyer demand. Once rates decline, competition will go up even more. If you want to get ahead of that and sell now, talk to a real estate agent.

Ways To Use Your Tax Refund If You Want To Buy a Home

Have you been saving up to buy a home this year? If so, you know there are a number of expenses involved – from your down payment to closing costs. But did you also know your tax refund can help you pay for some of these expenses? As Credit Karma explains:

“If one of your goals is to stop renting and buy a home, you’ll need to save up for closing costs and a down payment on the mortgage. A tax refund can give you a start on the road to homeownership. If you’ve already started to save, your tax refund could move you down the road faster.”

While how much money you may get in a tax refund is going to vary, it can be encouraging to have a general idea of what’s possible. Here’s what CNET has to say about the average increase people are seeing this year:

“The average refund size is up by 6.1%, from $2,903 for 2023’s tax season through March 24, to $3,081 for this season through March 22.”

Sounds great, right? Remember, your number is going to be different. But if you do get a refund, here are a few examples of how you can use it when buying a home. According to Freddie Mac:

- Saving for a down payment – One of the biggest barriers to homeownership is setting aside enough money for a down payment. You could reach your savings goal even faster by using your tax refund to help.

- Paying for closing costs – Closing costs cover some of the payments you’ll make at closing. They’re generally between 2% and 5% of the total purchase price of the home. You could direct your tax refund toward these closing costs.

- Lowering your mortgage rate – Your lender might give you the option to buy down your mortgage rate. If affordability is tight for you at today’s rates and home prices, this option may be worth exploring. If you qualify for this option, you could pay upfront to have a lower rate on your mortgage.

The best way to get ready to buy a home is to work with a team of trusted real estate professionals who understand the process and what you’ll need to do to be ready to buy.

Bottom Line

Your tax refund can help you reach your savings goal for buying a home. Connect with a local real estate professional about what you’re looking for, because your home may be more within reach than you think.

The Perks of Downsizing When You Retire [INFOGRAPHIC]

Some Highlights

- If you’re about to retire, or just did, downsizing can be a good way to try to cut down on some of your expenses.

- Smaller homes typically have lower energy and maintenance costs. Plus, you may have enough equity built up to fuel your move.

- If you’re thinking about moving to a smaller home, connect with a real estate professional to go over your goals and look at your options in the local market.

Builders Are Building Smaller Homes

There’s no arguing it, affordability is still tight. And if you’re trying to buy a home, that may mean you need to look at smaller houses to find one that’s still in your budget. But there is a silver lining: builders are focused on building these smaller homes right now and they’re offering incentives. And that can help give you more options that fit the bill.

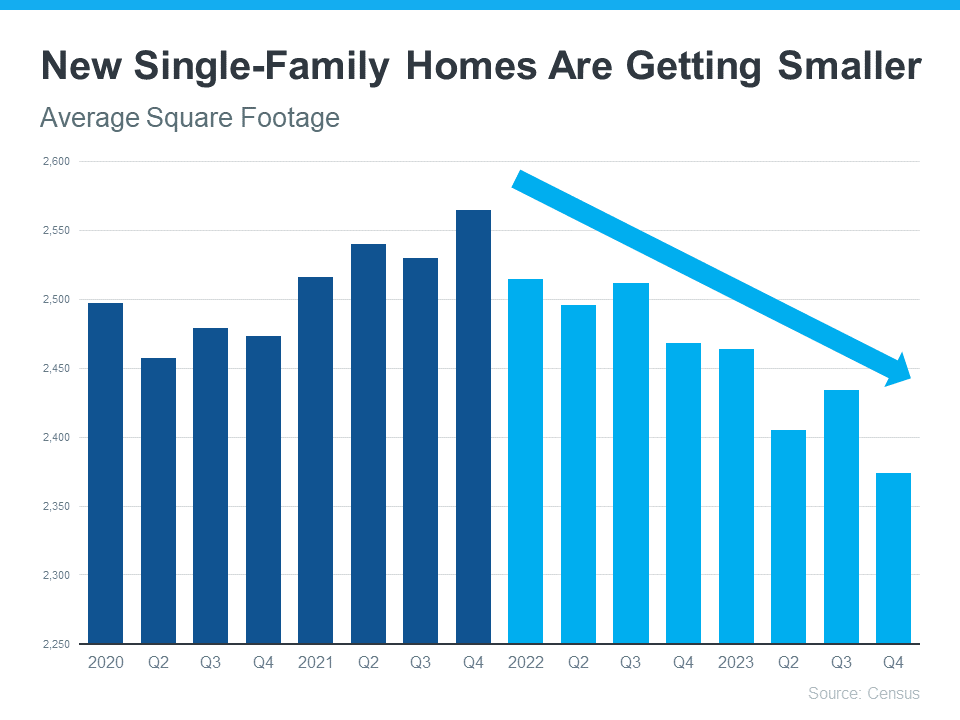

Newly Built Homes Are Trending Smaller

During the pandemic, homebuyers wanted (and could afford) larger homes – and builders delivered. They focused on homes that were bigger, so people had more space for things like working from home, having a home gym, bonus rooms for virtual school, and more.

But with the affordability challenges buyers are facing today, builders are increasingly shifting their attention to bringing smaller single-family homes to the market. The graph below uses data from the Census to show how this trend has evolved over the last few years:

So, why the shift to less square footage? It’s simple. Builders want to build what they know will sell. Basically, they focus on where the demand is strongest. And once mortgage rates started climbing and consumers felt the challenges of affordability creeping in, it became clear there was (and is) a very real need for smaller homes. As the National Association of Home Builders (NAHB) explains:

“After a brief increase during the post-covid building boom, home size is trending lower and will likely continue to do so as housing affordability remains constrained.”

A recent article in the Real Deal says this about how this helps buyers:

“Even a slightly smaller home can be thousands of dollars cheaper — for both builders and buyers. . . In response to affordability challenges, major homebuilders are shifting priorities away from the big ticket homes and towards the cheaper set.”

What This Means for You

If you’re having a hard time finding something in your budget, it may help to look at smaller homes. And, if you consider new builds specifically, you may find a few other fringe benefits that can help on the affordability front – like price reductions or mortgage rate buy-downs. As NAHB says:

“More than one-third of builders cut home prices in 2023. NAHB expects builders to continue offering smaller homes and more affordable designs as housing affordability remains a barrier to homeownership.”

As Charlie Bilello, Chief Market Strategist, at Creative Planning, explains:

“Homebuilders are adapting to the lowest affordability on record by building smaller homes and offering more incentives/price cuts. The median square footage of a new single-family home in the US has moved down to its lowest level since 2010.”

If you explore these options, you’ll also get brand new everything, enjoy a house with fewer maintenance needs, and some of the latest features available. That’s worth looking into, right?

Bottom Line

Builders building smaller homes can give you more affordable options at a time when you really need it. If you’re hoping to buy a home soon, partner with a local real estate agent to find out what’s available in your area.

Should I Move with Today’s Mortgage Rates?

When mortgage rates spiked up over the last few years, some homeowners put their plans to move on pause. Maybe you did too because you didn’t want to sell and take on a higher mortgage rate for your next home. But is that still the right strategy for you?

In today’s market, data shows more homeowners are getting used to where rates are and thinking it may be time to move. As Mark Zandi, Chief Economist at Moody’s Analytics, explains:

“Listings are up a bit as life events and job changes are putting increasing pressure on locked-in homeowners to sell their homes. Homeowners may also be slowly coming to the realization that mortgage rates aren’t going back anywhere near the rate on their existing mortgage.”

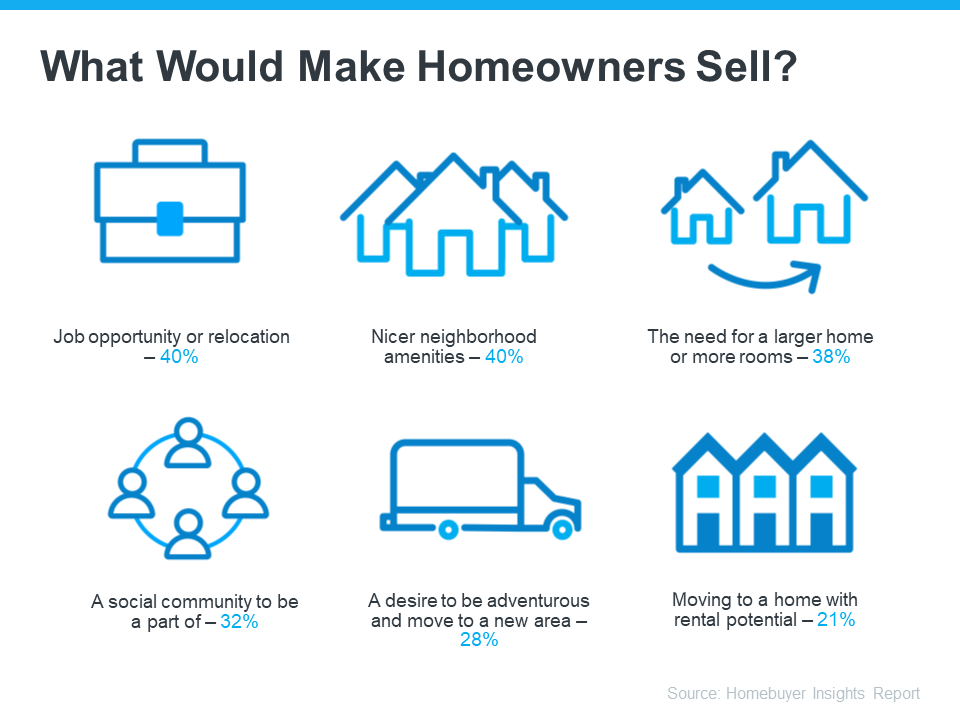

A recent study from Bank of America sheds light on some of the things homeowners say would make them sell, even with rates where they are right now (see visual below):

What Would Motivate You To Move?

Now that you know why other people would move, take a minute to think about what would make a move worth it for you. Is it time to take a chance and go for your dream job, even though it’s not local? Are you looking for a neighborhood that has more to offer and a close-knit sense of community? Maybe you just need more space, you’re looking for your next great adventure, or you want a house that opens up rental opportunities to pad your income.

And here’s something else to consider. Mortgage rates are still expected to go down over the course of the year. And once that happens, there’s going to be a big rush of buyers jumping back into the market. While you could delay your plans until rates drop, you’ll only have more competition with those buyers if you do.

So, does that mean it’s worth it to move now, even with rates where they are? The answer is: that it depends.

You’ll want to consider today’s mortgage rates, where they’re expected to go from here, and what would prompt you to want to make a change as you decide on your next steps. An expert can help with that.

Bottom Line

Other homeowners are getting used to rates and deciding to move. Talk to a local real estate agent to go over what matters most to you and if it’s time for you to jump back into the market too.

The Top 5 Reasons You Need a Real Estate Agent when Buying a Home

You may have heard headlines in the news lately about agents in the real estate industry and discussions about their commissions. And if you’re following along, it can be pretty confusing. But here’s the thing you really need to know – expert advice from a trusted real estate agent is priceless, now more than ever. And here’s why.

A real estate agent does a lot more than you may realize.

Your agent is the person who will guide you through every step when buying a home and look out for your best interests along the way. They smooth out a complex process and take away the bulk of the stress of what’s likely your largest purchase ever. And that’s exactly what you want and deserve.

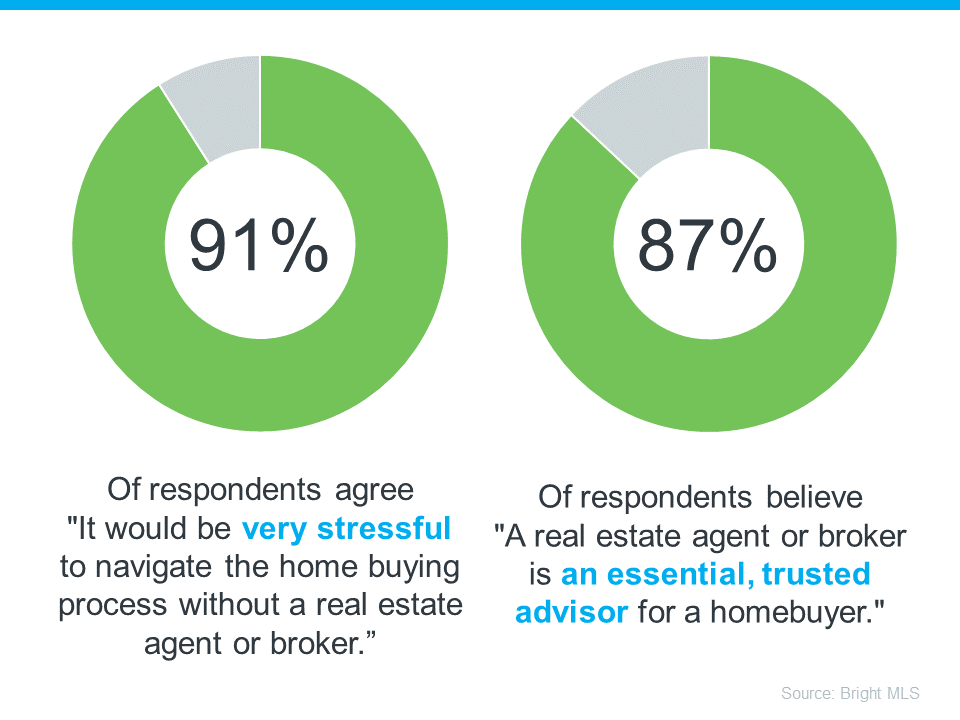

This is at least a part of the reason why a recent survey from Bright MLS found an overwhelming majority of people agree an agent is a key part of the homebuying process (see visual below):

To give you a better idea of just a few of the top ways agents add value, check out this list.

1. Deliver Industry Experience

The right agent – the professional – will coach you through everything from start to finish. With professional training and expertise, agents know the ins and outs of the buying process. And in today’s complex market, the way real estate transactions are executed is constantly changing, so having the best advice on your side is essential.

2. Provide Expert Local Knowledge

In a world that’s powered by data, a great agent can clarify what it all means, separate fact from fiction, and help you understand how current market trends apply to your unique search. From how quickly homes are selling to the latest listings you don’t want to miss, they can explain what’s happening in your specific local market so you can make a confident decision.

3. Explain Pricing and Market Value

Agents help you understand the latest pricing trends in your area. What’s a home valued at in your market? What should you think about when you’re making an offer? Is this a house that might have issues you can’t see on the surface? No one wants to overpay, so having an expert who really gets true market value for individual neighborhoods is priceless. An offer that’s both fair and competitive in today’s housing market is essential, and a local expert knows how to help you hit the mark.

4. Review Contracts and Fine Print

In a fast-moving and heavily regulated process, agents help you make sense of the necessary disclosures and documents, so you know what you’re signing. Having a professional that’s trained to explain the details could make or break your transaction, and is certainly something you don’t want to try to figure out on your own.

5. Bring Negotiation Expertise

From offer to counteroffer and inspection to closing, there are a lot of stakeholders involved in a real estate transaction. Having someone on your side who knows you and the process makes a world of difference. An agent will advocate for you as they work with each party. It’s a big deal, and you need a partner at every turn to land the best possible outcome.

Bottom Line

Real estate agents are specialists, educators, and negotiators. They adjust to market changes and keep you informed. And keep in mind, every time you make a big decision in your life, especially a financial one, you need an expert on your side.

Expert advice from a trusted professional is priceless. Connect with a local real estate agent today.

Don’t Let Your Student Loans Delay Your Homeownership Plans

If you have student loans and want to buy a home, you might have questions about how your debt affects your plans. Do you have to wait until you’ve paid off those loans before you can buy your first home? Or is it possible you could still qualify for a home loan even with that debt? Here’s a look at the latest information so you have the answers you need.

A Bankrate article explains:

“Roughly 60 percent of U.S. adults who have held student loan debt have put off making important financial decisions due to that debt . . . For Gen Z and millennial borrowers alone, that number rises to 70 percent.”

This includes one of the biggest financial decisions you’ll ever make, buying a home. But you should know, even with student loans, waiting to buy a home may not be necessary. While everyone’s situation is unique, your goal may be more within your reach than you realize. Here’s why.

Can You Qualify for a Home Loan if You Have Student Loans?

According to an annual report from the National Association of Realtors (NAR), 38% of first-time buyers had student loan debt and the typical amount was $30,000.

That means other people in a similar situation were able to qualify for and buy a home even though they also had student loans. And you may be able to do the same, especially if you have a steady source of income. As an article from Bankrate says:

“. . . you can have student loans and a mortgage at the same time. . . . If you have student loans and want a mortgage, there are multiple home loan programs you might qualify for . . .”

The key takeaway is, for many people, homeownership is achievable even with student loans.

You don’t have to figure this out on your own. The best way to make a decision about your goals and next steps is to talk to the professionals. A trusted lender can walk you through your options based on your situation, and share what’s worked for other buyers.

Bottom Line

Lots of other people with student loan debt are able to buy their own homes. Talk to a lender to go over your options and see how close you are to reaching your goal.

Top 5 Reasons To Hire an Agent When Buying a Home [INFOGRAPHIC]

Some Highlights

- Hiring an agent when buying a home helps you understand the buying process and the local market.

- They’ll also go over contracts and fine print with you, so you understand what you’re agreeing to. Plus, they’re good at negotiating, making sure you get the best deal.

- Expert advice from a trusted real estate professional is priceless. Connect with a local agent today.

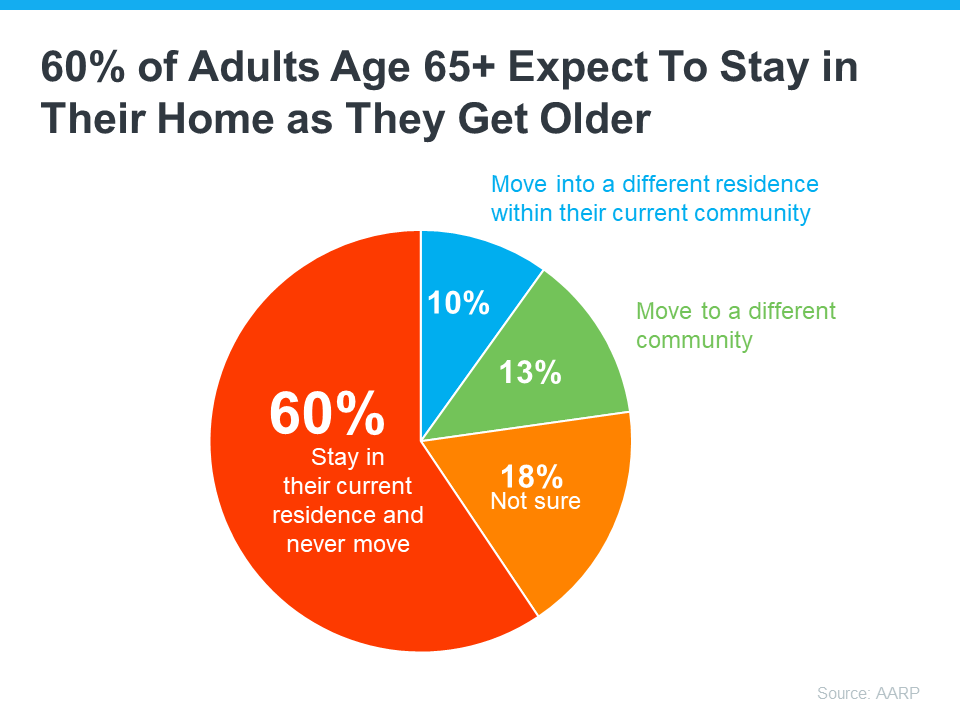

Boomers Moving Will Be More Like a Gentle Tide Than a Tsunami

Have you heard the term “Silver Tsunami” getting tossed around recently? If so, here’s what you really need to know. That phrase refers to the idea that a lot of baby boomers are going to move or downsize all at once. And the fear is that a sudden influx of homes for sale would have a big impact on housing. That’s because it would create a whole lot more competition for smaller homes and would throw off the balance of supply and demand, which ultimately would impact home prices.

But here’s the thing. There are a couple of faults in that logic. Let’s break them down and put your mind at ease.

Not All Baby Boomers Plan To Move

For starters, plenty of baby boomers don’t plan on moving at all. A study from the AARP says more than half of adults aged 65 and older want to stay in their homes and not move as they age (see graph below):

While it’s true circumstances may change and some people who don’t plan to move (the red in the chart above) may realize they need to down the road, the vast majority are counting on aging in place.

As for those who stay put, they’ll likely modify their homes as their needs change over time. And when updating their existing home won’t work, some will buy a second home and keep their original one as an investment to fuel generational wealth for their loved ones. As an article from Inman explains:

“Many boomers have no desire to retire fully and take up less space . . . Many will modify their current home, and the wealthiest will opt to have multiple homes.”

Even Those Who Do Move Won’t Do It All at Once

While not all baby boomers are looking to sell their homes and move – the ones who do won’t all do it at the same time. Instead, it’ll happen slowly over many years. As Freddie Mac says:

“We forecast the ‘tsunami’ will be more like a tide, bringing a gradual exit of 9.2 million Boomers by 2035 . . .”

As Mark Fleming, Chief Economist at First American, says:

“Demographics are never a tsunami. The baby boomer generation is almost two decades of births. That means they’re going to take about two decades to work their way through.”

Bottom Line

If you’re stressed about a Silver Tsunami shaking the housing market overnight, don’t be. Baby boomers will move slowly over a much longer period of time.

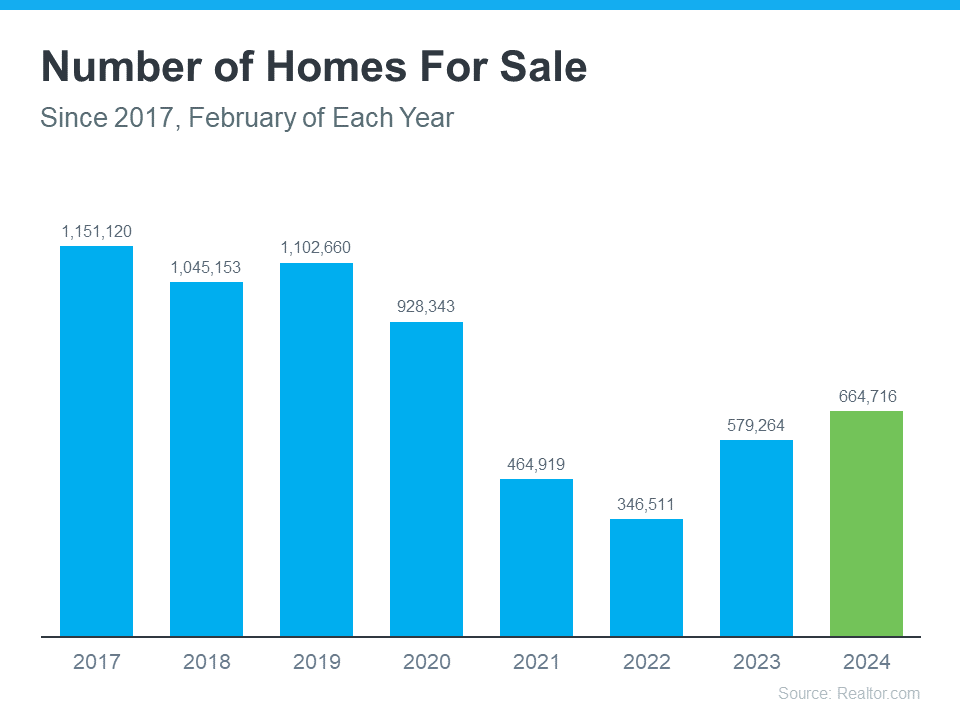

Newly Built Homes Could Be a Game Changer This Spring

Buying a home this spring? You’re probably navigating today’s affordability challenges and dealing with the limited number of homes for sale. But, what if there was a solution that could help with both?

If you’re having a hard time finding a home you love, and mortgage rates are putting pressure on your budget, it may be time to look at newly built homes. Here’s why.

New Home Construction Is an Inventory Bright Spot

When looking for a home, you can choose between existing homes (those that are already built and previously owned) and newly constructed ones. While the number of existing homes for sale has increased this year, there are still fewer available than there were in more typical years in the housing market, like back in 2018 or 2019.

So, if you’re looking to expand your pool of options even more, turning to newly built homes can help. As Danielle Hale, Chief Economist at Realtor.com, explains:

“The shortage of existing homes For Sale has opened up the possibility of new-home construction to more buyers who may not have once considered it.”

And the good news is, there are more newly built homes to pick from right now. The graphs below use data from the Census to show how new home construction is ramping up in two key areas (see most recent spike in green):

Starts, or homes where builders just broke ground, have seen a big increase lately. And completions, homes that builders just finished, are also up significantly. So, if you want a new, move-in ready home or you want to get in early and customize your build along the way, you have more options right now.

Builders Are Offering Incentives To Help with Affordability

And to sweeten the pot, builders are offering things like mortgage rate buy-downs and other perks for homebuyers right now. This can help offset today’s affordability challenges while also getting you into your dream home. Mark Fleming, Chief Economist at First American, explains why you may find builders have more wiggle room to offer more for you than the typical homeowner:

“Builders aren’t rate locked-in. They would love to sell you the home because they’re not living in it. It costs money not to sell the home. And many of the public home builders have said in their earnings calls that they are not going to be pulling back on incentives, especially the mortgage rate buydown, so that will help the new-home market continue to perform well in the spring home-buying season.”

An article from HousingWire also says this about what builders are offering right now:

“. . . the use of sales incentives still shows some momentum as 60% of respondents reported using them, up from 58% in February. “

Just remember, buying from a builder is different from buying from a home seller, so it’s important to partner with a local real estate agent. Builder contracts can be complex. A trusted agent will be your advocate throughout the process.

They’ll be your go-to resource for advice on construction quality and builder reputation, reviewing and negotiating contracts to get you the best deal, helping you decide on which customizations and upgrades are most worthwhile, and a whole lot more.

Bottom Line

If you’re struggling to find a home to buy, or with today’s affordability challenges, connect with a local real estate agent to see if newly built homes could be the solution you’re looking for.