Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

When planning a move, a newly built home might not be the first thing that comes to mind. However, with more homes for sale in the Greater Cincinnati, Northern Kentucky, and Southeast Indiana areas—including brand-new options—and builders focusing on smaller, more affordable designs, these new builds may be the key to achieving your real estate goals.

Why Consider a Newly Built Home?

Here’s why a newly built home could be the perfect fit for you—and how an agent can help if you’re thinking, “I want to sell my house and move into something new.”

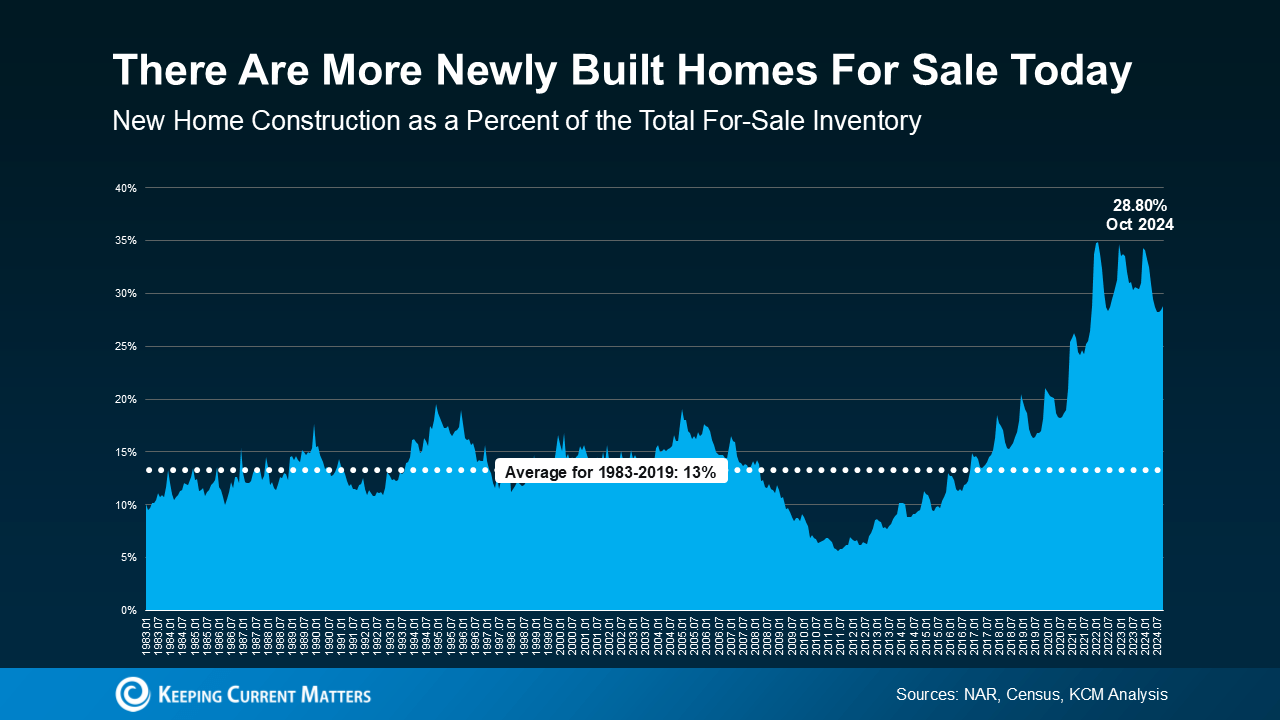

1. More Newly Built Homes Are Available

First, let’s break down the types of homes for sale today. A newly built home is either under construction or just completed, while an existing home is one that’s been previously lived in.

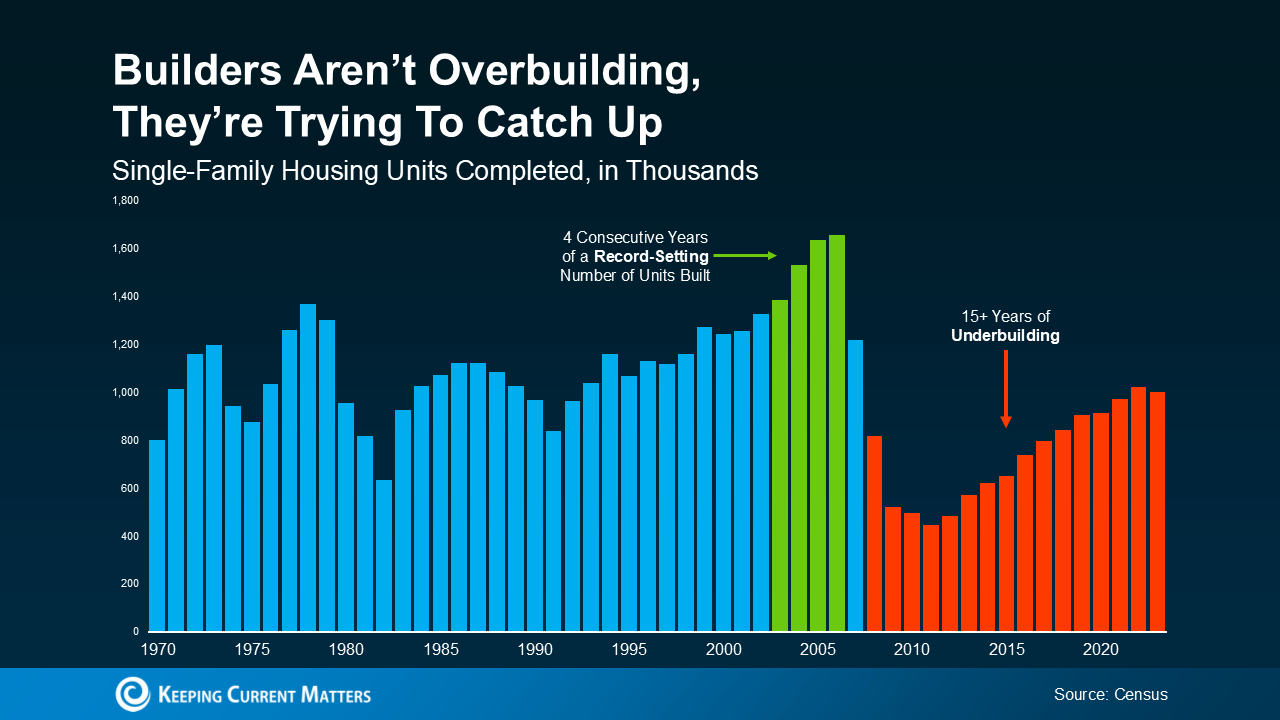

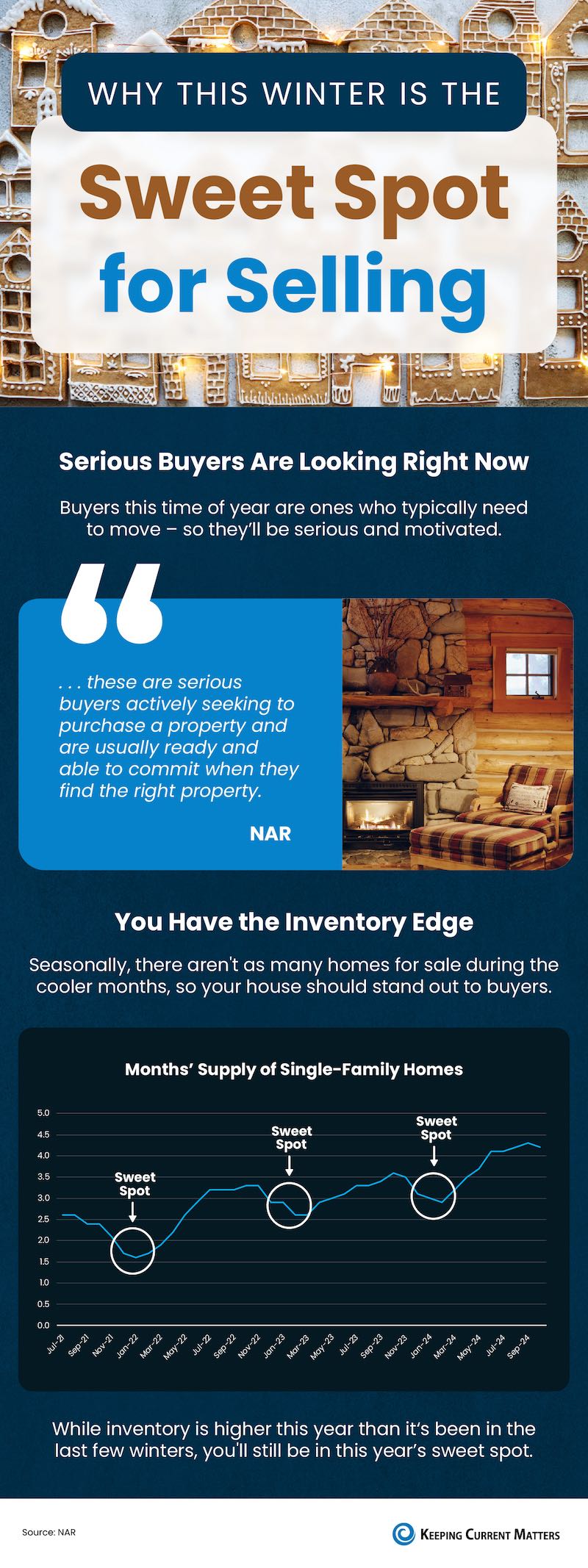

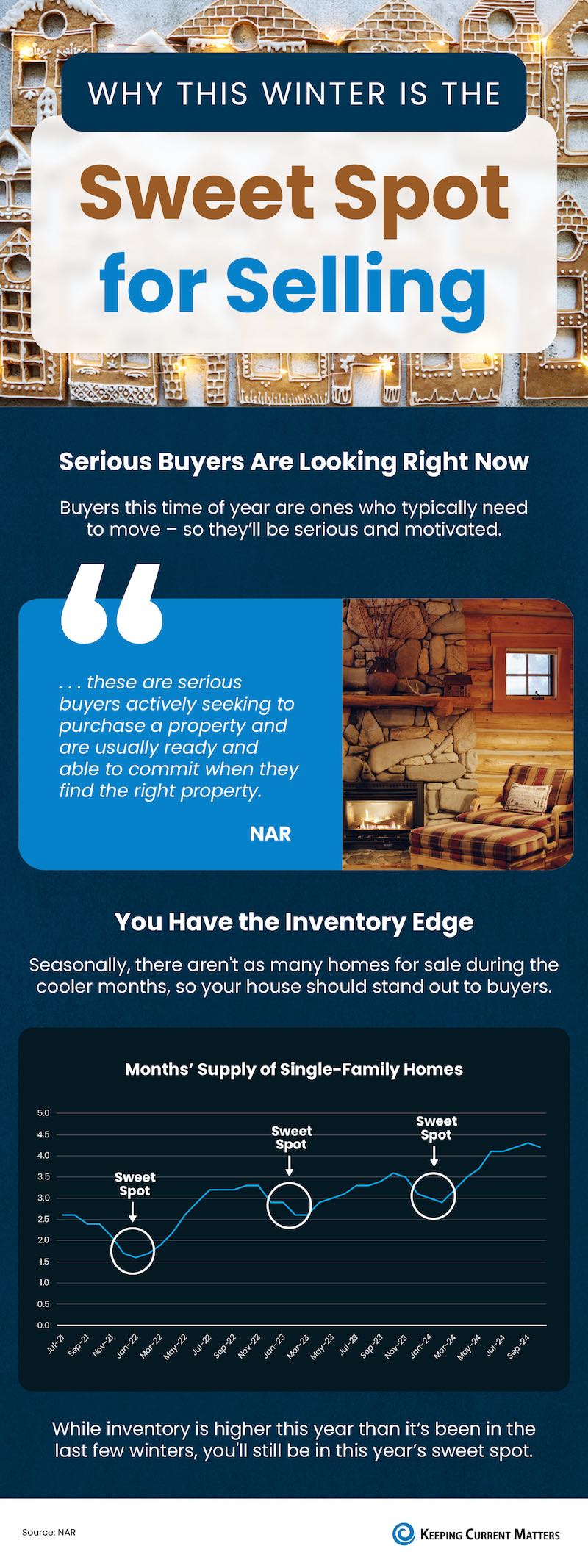

Currently, the inventory of existing homes for sale remains low. If you’re finding it hard to locate the right fit, expanding your search to include new builds can significantly increase your options. Right now, newly built homes represent a larger share of the market than in previous years, accounting for 28.8% of all inventory (see graph below):

From 1983 to 2019, newly built homes made up only 13% of the total inventory. Today, thanks to increased construction activity, they now represent nearly one-third of all homes on the market.

Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), explains:

“Even though existing home sales have been stuck at low levels, newly constructed home sales look to mark one of their best annual performances in 15 years. The new home inventory has been consistently rising with homebuilders getting active, making up around 1/3 of total inventory.”

Builders are addressing the demand created by years of underbuilding. While demand for homes remains high, the growing availability of new builds offers more opportunities for buyers in the real estate market.

2. Newly Built Homes Are Becoming More Affordable

Still wondering if a new build fits your budget? The good news is that the average cost of newly built homes has actually decreased compared to a year ago.

Why is this happening? Builders are focusing on affordability by designing smaller homes with lower price points, making them more accessible to today’s buyers. As Realtor.com notes:

“Builders are increasingly bringing smaller, more affordable homes to the market, so buyers may find more newly built homes that fit their budget.”

Keep in mind that buying a newly built home is different from purchasing an existing property. Builder contracts often have unique terms, so partnering with a local real estate expert who understands these nuances is essential.

Bottom Line

If you’re searching for homes for sale in Greater Cincinnati, Northern Kentucky, or Southeast Indiana, a new build might be the ideal opportunity to achieve your goals. Whether you’re exploring new homes or thinking, “I’m ready to sell my house,” a knowledgeable real estate agent can guide you through the process and help you find the perfect fit for your needs and budget.