Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

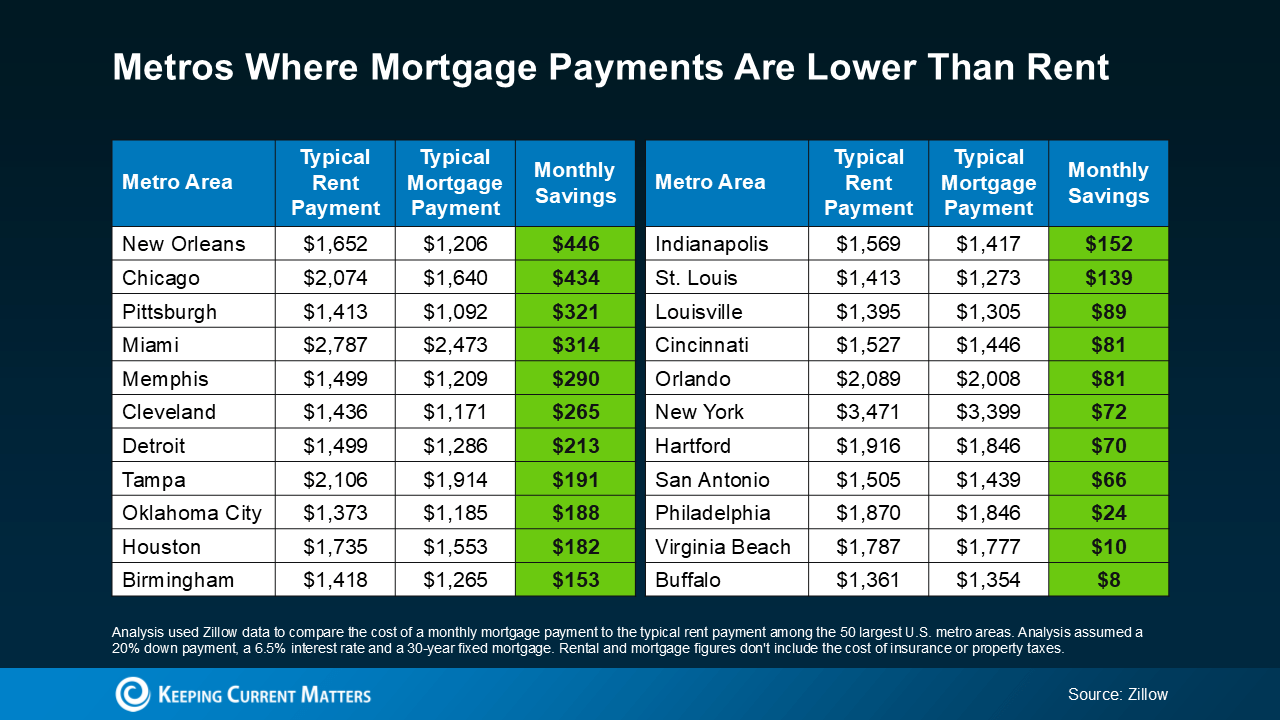

Buying Beats Renting in 22 Major U.S. Cities

That’s right—according to a recent study from Zillow, in 22 of the 50 largest metro areas, monthly mortgage payments are now lower than rent payments (see chart below):

As mortgage rates have eased off their recent peak, home prices have moderated, and inventory has ticked up, affordability has improved significantly. When you add all of that up, it’s getting less expensive to buy a home than to rent one in many parts of the country.

As mortgage rates have eased off their recent peak, home prices have moderated, and inventory has ticked up, affordability has improved significantly. When you add all of that up, it’s getting less expensive to buy a home than to rent one in many parts of the country.

This is a big deal if you’ve been renting for a while now. But if you don’t see your city on this list, don’t sweat it. Things are moving fast, and your area might be joining these top metros soon.

You see, talking with a local real estate agent about what’s happening in your market before this happens in your ideal neighborhood could really change the game for you. It’s all about being informed by a true expert, and understanding what was out of reach before might actually be getting more affordable than you think.

Now, while this study compares monthly rent to principal and interest on a mortgage payment (not the whole monthly payment), let’s think through this. As Zillow notes, what you can’t ignore when you buy a home are things like taxes, insurance, utilities, and maintenance that should also be factored into your budget and your monthly payment.

But remember – renters pay extra fees too, like renters’ insurance, utilities, parking, and more. And while doing the math may feel like a drag, this equation could be a much more exciting one to work through today.

So, grab your calculator and your agent because the big takeaway is this: it may be time to determine if you’re in a spot to afford what you couldn’t just a few months ago.

As Orphe Divounguy, Senior Economist at Zillow, says:

“… for those who can make it work, homeownership may come with lower monthly costs and the ability to build long-term wealth in the form of home equity — something you lose out on as a renter. With mortgage rates dropping, it’s a great time to see how your affordability has changed and if it makes more sense to buy than rent.”

Whether you live in one of these budget-friendly metros where the scales have already tipped in your favor, or any town in-between, it’s time to connect with a local real estate agent to get the conversation started.

With mortgage rates coming down and more homes hitting the market, you’ll want to be ready to jump back into your search – before everyone else does.

Bottom Line

If you’re tired of renting and ready to find out what it takes to purchase a home in your area now that the landscape may be shifting, connect with a local real estate agent to do the math and see if buying a home makes sense for you now or sometime soon.

Buy Now, or Wait?

Some Highlights

- If you’re wondering if you should buy now or wait, here’s what you need to know.

- If you wait for rates to drop more, you’ll have to deal with more competition and higher prices as additional buyers jump back in. But if you buy now, you’d get ahead of that and have the chance to start building equity.

- Should you buy now or wait? Connect with a real estate agent and talk through it together, so you can make your best decision.

Don’t Fall for These Real Estate Agent Myths

When it’s time to buy or sell a home, one of the most important decisions you’ll make is who you’ll work with as your agent. That choice will have an impact on your entire experience and how smoothly it goes.

As you figure out who you’ll partner with, it’s important to know what to expect and what to look for. Unfortunately, there may be some myths holding you back from making the best decision possible. So, let’s take some time to address those, and make sure you have the information you need to find the right agent for you.

Myth #1: All Real Estate Agents Are the Same

You might think all agents are the same – so it doesn’t matter who you work with. But, in reality, agents have varying levels of experience, specialties, and market knowledge, which can have a big impact on your results. For example: you’ll get much better service and advice from someone who is a true expert in their field. As Business Insider explains:

“If you were planning to get your hair done for a special event, you’d want to visit a stylist who specifically has experience doing that type of work — you wouldn’t make an appointment with someone who primarily does kids’ hair. The same concept applies to finding a real estate agent. If you have a smaller budget, you probably don’t want to work with an agent who exclusively sells multimillion-dollar properties.”

Take some time to talk with each agent you’re considering. Ask about their experience level and what they specialize in. This will help you find the one that’s the best fit for your search.

Myth #2: You Can Save Money by Not Using an Agent

As a seller, you may think you can save money by not working with a pro. However, the expertise, negotiation skills, and market knowledge an agent provides generally saves you money and helps you avoid making costly mistakes. Without that guidance, you could find yourself doing something like overpricing your house. And that’s a misstep that’ll cost you when it sits on the market for far too long. That’s why U.S. News Real Estate says:

“When it comes to buying or selling your home, hiring a professional to guide you through the process can save you money and headaches. It pays to have someone on your side who’s well-versed in the nuances of the market and can help ensure you get the best possible deal.”

Myth #3: Agents Will Push You To Spend More

You may also be worried an agent will push you to buy a more expensive house in order to increase their commission. But that’s not how that should go. A good agent will respect your budget and work hard to find a home that truly fits your financial situation and needs. With their market know-how, they’ll point you toward the best option for you, rather than try to pad their own pockets on your dime. As NerdWallet explains:

“Among other things, a good buyer’s agent will find homes for sale. A buyer’s agent will help you understand the type of home you can afford in the current market, find listed homes that match your needs and price range, and then help you narrow the options to the properties worth considering.”

Myth #4: Market Conditions Are the Same Everywhere, So Why Do I Need a Pro?

Maybe you believe housing market conditions are the same no matter where you are. But that couldn’t be further from the truth. Real estate markets are highly localized, and conditions can vary widely from one area to another. This is why you can’t pick just anyone you find online. You should choose an agent who’s an expert on your specific local market. As a recent article from Bankrate says:

“Real estate is very localized, and you want someone who’s extremely knowledgeable about the market in your specific area.”

You’ll know you’ve found the right person when they can explain the national trends and how your area stacks up too. That way you’re guaranteed to get the full picture when you ask: “how’s the market?”

Bottom Line

Don’t let myths keep you from the expert guidance you deserve. With market knowledge and top resources, a trusted local real estate agent isn’t just helpful, they’re invaluable.

In what could be one of the biggest financial decisions of your life, having the right pro by your side is a game changer. Connect with an agent to make sure you get the best outcome possible.

Why Buying Now May Be Worth It in the Long Run

Should you buy a home now or should you wait? That’s a question a lot of people have these days. And while what’s right for you is going to depend on a lot of different factors, here’s something you’ll want to consider as you make your decision.

As soon as you buy, you’ll start gaining equity. And you’d be surprised how quickly that can add up – even with more moderate home price appreciation.

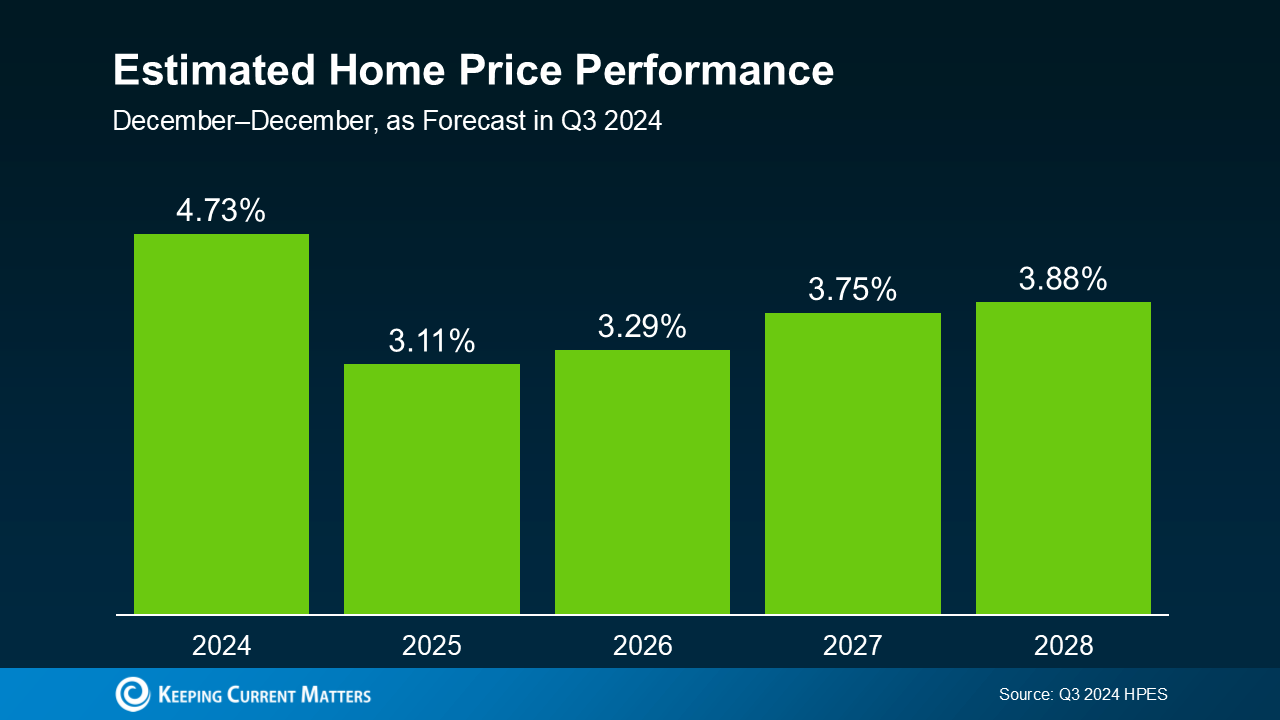

Each quarter, Fannie Mae releases the Home Price Expectations Survey. It asks over one hundred economists, real estate experts, and investment and market strategists what they forecast for home prices over the next five years. In the latest release, experts project prices will continue to rise nationally through at least 2028 (see the graph below):

While home prices are going to vary from one local area to the next, this shows they’re expected to keep going up nationally. The size of the increase varies from year-to-year, but the important takeaway is that prices are forecast to rise every single year – just at a moderate pace.

While home prices are going to vary from one local area to the next, this shows they’re expected to keep going up nationally. The size of the increase varies from year-to-year, but the important takeaway is that prices are forecast to rise every single year – just at a moderate pace.

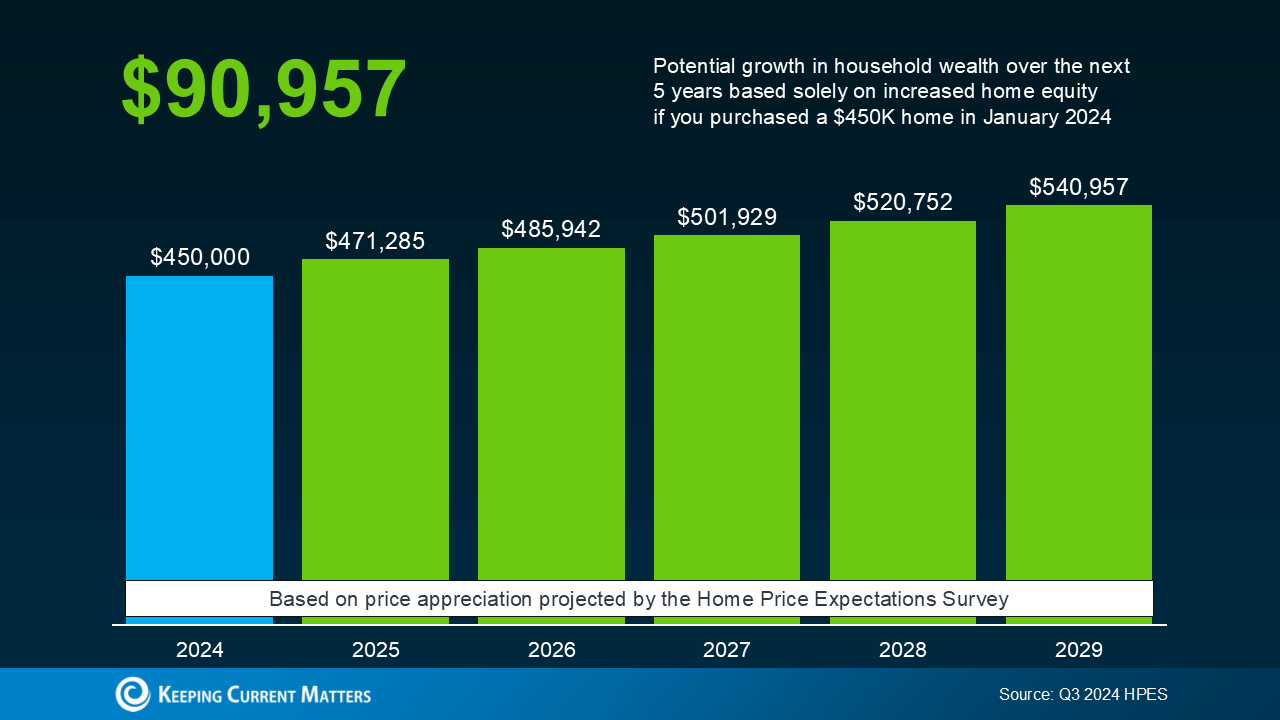

And while rising home prices may not sound great right now, once you own a home, that growth will be a big bonus for you. Here’s a look at what you stand to gain equity-wise once you buy. The graph below uses a typical home’s value and those HPES projections to show how much equity is at stake:

If you bought a $450,000 home at the beginning of this year, based on that starting value and the expert forecasts from the HPES, you could gain more than $90,000 in household wealth over the next five years. That’s significant.

If you bought a $450,000 home at the beginning of this year, based on that starting value and the expert forecasts from the HPES, you could gain more than $90,000 in household wealth over the next five years. That’s significant.

So, if you’re ready and able to buy, and growing your wealth is important to you, you’ve got an opportunity in front of you. And now that mortgage rates have fallen, it may be time to consider making a move.

To talk more about your options and what makes sense, lean on a pro. They’ll be able to tell you what home prices are doing in your area and what that means for your move (and your future equity). The Mortgage Reports says:

“Given the intricacies of the current market, it’s more important than ever to stay informed and up to date about housing market conditions. Whether you’re looking to buy or sell in the remaining months of 2024, having a professional guide you through the process can make all the difference.”

Bottom Line

The decision to buy now or wait is a very personal one, but it’s valuable to have an expert’s perspective. They won’t push you, but they will explain things you may not have considered, like the equity that’s at stake.

If you want help weighing your options and thinking through how the current market factors in, connect with a local real estate agent.

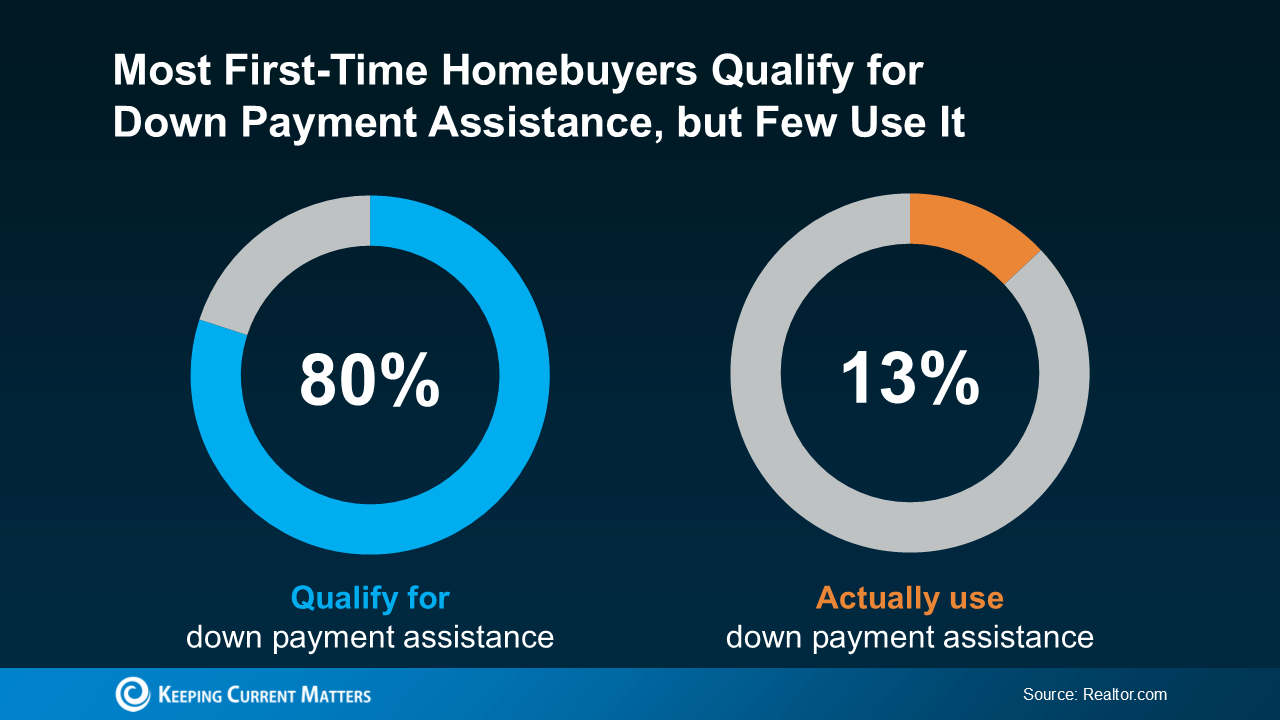

The Down Payment Assistance You Didn’t Know About

Believe it or not, almost 80% of first-time homebuyers qualify for down payment assistance, but only 13% actually use it. And if you’re hoping to buy a home, this is a mission-critical gap to close – fast (see graph below):

Here’s what you need to know to maximize your down payment in today’s housing market in Cincinnati and Northern Kentucky.

Amplify Your Down Payment Potential in Cincinnati and Northern Kentucky

For first-time buyers in Cincinnati, Northern Kentucky, and the surrounding communities, it’s important to explore all the resources available to help with your down payment. Many of these resources can help you reach your goal faster than you might expect.

For example, there are loan options available in the Cincinnati and Northern Kentucky areas that require as little as 3% down, or even 0% for certain qualified borrowers, like Veterans. Don’t forget about the down payment assistance programs specific to this region, such as grants and other local opportunities, which can help cover your upfront costs.

If you’re interested in learning more about these programs and how they can benefit you in the Cincinnati or Northern Kentucky housing markets, connecting with a trusted local lender is key. Failing to explore these options could mean leaving money on the table and missing out on your dream home in the region. A higher down payment can reduce your monthly mortgage payment and even help avoid or reduce fees like private mortgage insurance.

Don’t Let News Headlines About Down Payments in Cincinnati and Northern Kentucky Scare You

You may have seen headlines about rising down payments across the country, and it’s true. According to Redfin:

“The typical down payment for U.S. homebuyers hit a record high of $67,500 in June, up 14.8% from $58,788 a year earlier . . . This was the 12th consecutive month the median down payment rose year over year.”

But don’t let this discourage you from purchasing a home in Cincinnati or Northern Kentucky. These rising averages don’t mean that down payment requirements are increasing. Instead, it reflects buyers choosing to put more down to offset higher mortgage rates or leveraging equity from the sale of their previous homes. As HousingWire explains:

“. . . buyers are putting down a higher percentage of the purchase price to lower their monthly mortgage payment. And buyers also had more equity from their home sales, which gives them more cushion.”

Here’s why:

- A bigger down payment can lower your monthly mortgage payment: In today’s market, affordability is a challenge for many buyers in the Cincinnati and Northern Kentucky areas. Those who can make larger down payments are doing so to reduce their future housing costs.

- Buyers with existing homes have record equity: Homeowners in Cincinnati and Northern Kentucky who purchased a few years ago have seen significant price appreciation. They are now able to use that equity to make larger down payments on their next homes, giving them an advantage over first-time buyers.

Bottom Line for Buyers in Cincinnati and Northern Kentucky

What’s the best step to take? Reach out to a trusted lender in Cincinnati or Northern Kentucky to explore your options. They can help you understand where you stand today and guide you to the resources that may be available to you in these thriving local markets. Help is available – all you need to do is work with a local pro to make the most of it.

Is Your House Priced Too High?

Every seller wants to get their house sold quickly, for as much money as they can, with as few headaches as possible. And chances are, you’re no different.

But did you know one of the biggest things that could jeopardize your success is the asking price for your home? Pricing your house correctly is one of the most crucial steps in the selling process.

So, how do you know if you’re missing the mark? Here are four signs your high asking price might be turning potential buyers away—and why leaning on your real estate agent is the best way to course correct.

1. You’re Not Getting Many Showings or Offers

One of the most obvious signs your house may be overpriced is a lack of showings. If it’s been on the market for several weeks and only a few buyers have come to see it—or worse, you haven’t gotten any offers—it could be a clear indication the price isn’t matching up with what buyers expect. Because buyers who have been looking for a while can easily spot (and write off) a home that seems overpriced.

Your real estate agent will coach you through this, so lean on their experience for what you may want to try to bring more buyers in, including considering a price cut.

2. Buyers Have Consistent Negative Feedback after Showings

And if after the showings you do have, comments from the potential buyers aren’t great, you may need to course correct. Feedback from showings is an important part of understanding how buyers see your house. If they consistently say it’s overpriced compared to other homes they’ve seen, it’s time to reconsider your pricing strategy.

Your agent will gather and analyze this feedback for you, so you can look at how your house stacks up in the market. They can also suggest specific improvements or staging changes to better justify your asking price, or recommend one that aligns with today’s buyer expectations. As the National Association of Realtors (NAR) explains:

“Based on all the data gathered, agents may make adjustments to the initial price recommendation. This could involve adjusting for market conditions, property uniqueness, or other factors that may impact the property’s value.”

3. It’s Been on the Market for Too Long

And that lack of interest is ultimately going to lead to it sitting on the market without any serious bites. The longer it lingers, the more likely it is to raise red flags for buyers, who may wonder if something is wrong with it. Especially in today’s market with growing inventory, a long listing period means your house is stale – and that makes it even harder to sell.

Your real estate agent will be able to give you perspective on how quickly other homes in your area are selling and walk you through what’s working for other sellers. That way you can decide together if there’s something you want to do differently. As a Bankrate article says:

“Check with your agent about the average number of days homes spend on the market in your area. If your listing has been up significantly longer than average, that may be a sign to reduce the price.”

4. Your Neighbor’s House Sold Without an Issue

And here’s the last one to watch out for. If similar homes in your area are selling faster than yours, it’s a clear sign that something is off. This could be due to things like a lack of upgrades, outdated features, or a less desirable location. Or, it may be priced too high.

Your agent will keep you up to date on your competition and what changes, if any, you need to make your home more competitive. They’ll offer advice on small updates that could increase your home’s appeal or how to adjust your strategy to reflect the reality of the market today.

Bottom Line

Pricing a home correctly is both an art and a science. It requires a deep understanding of the market and buyer psychology. And when the price isn’t drawing in buyers, there’s no better resource than your agent on what you may want to do next.

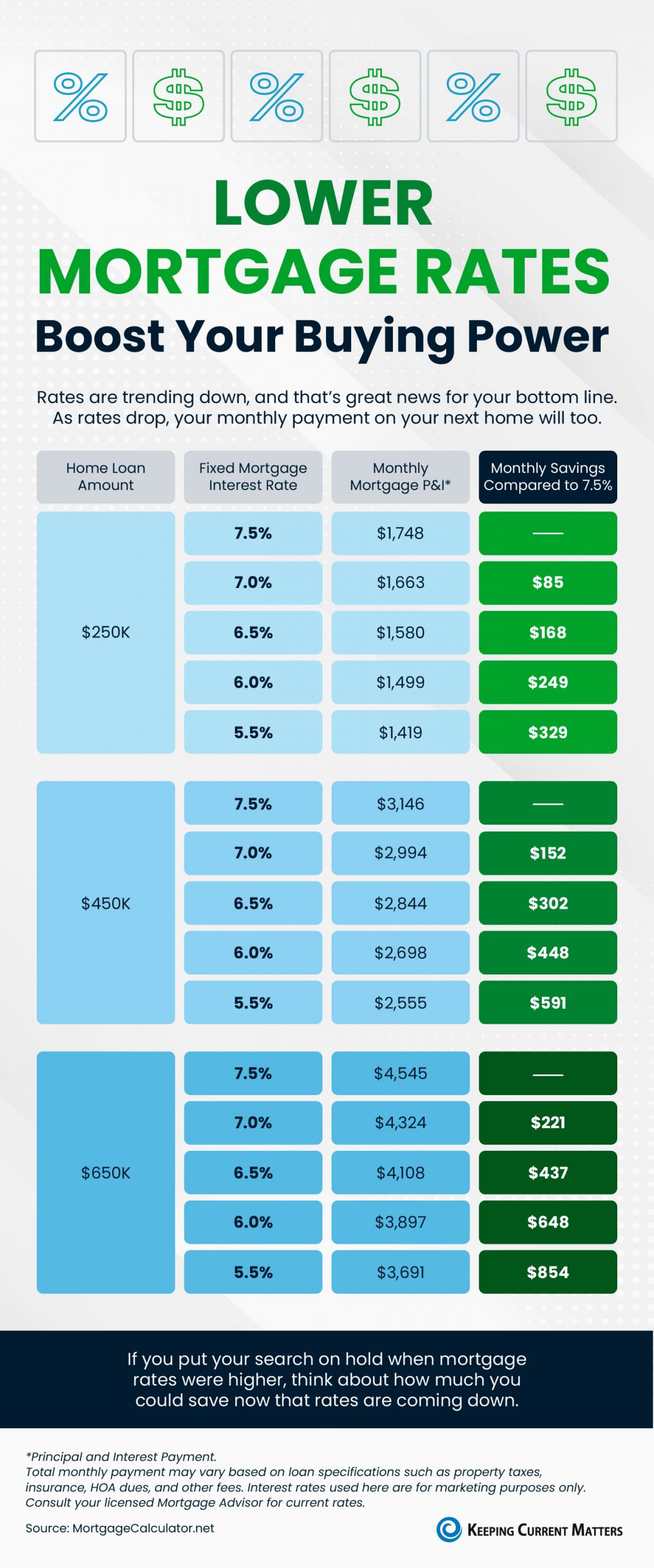

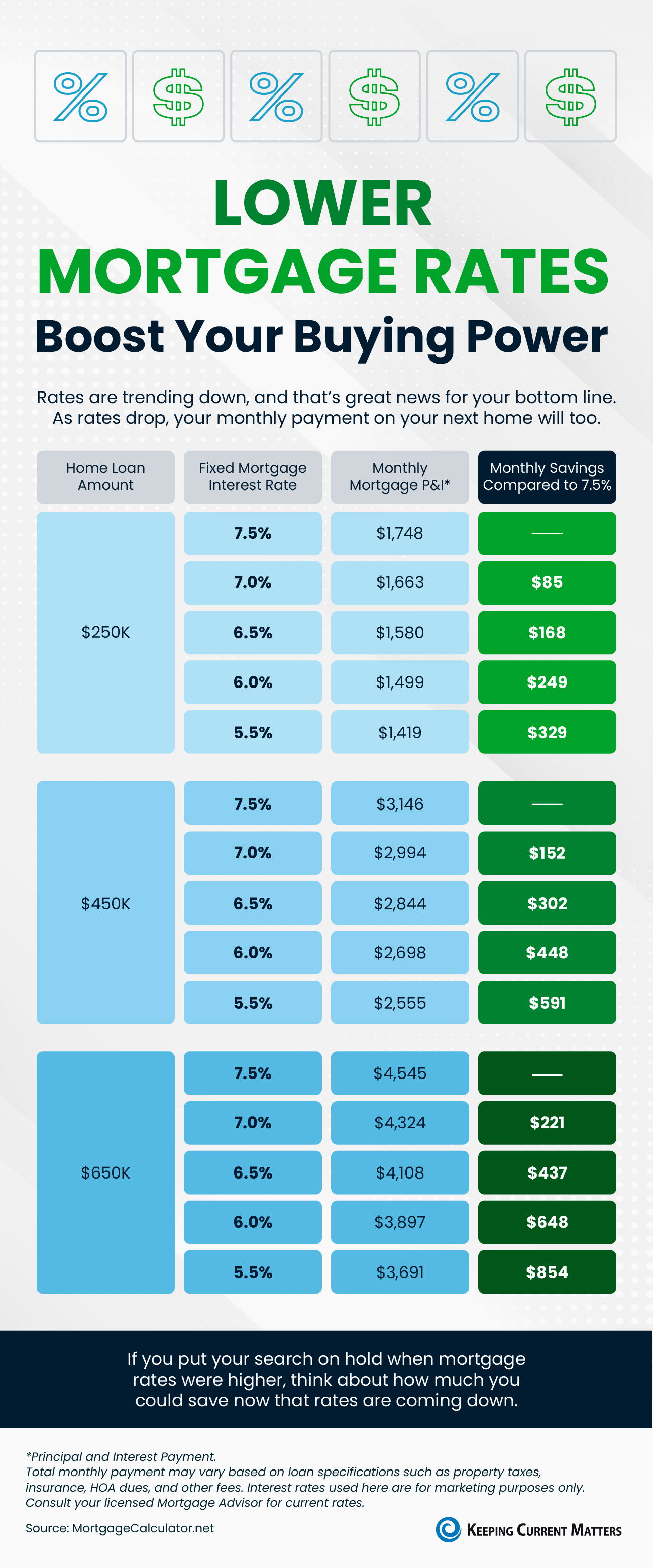

Lower Mortgage Rates Boost Your Buying Power

Some Highlights

- Mortgage rates are trending down and that’s great news for your bottom line.

- As rates drop, your monthly payment on your next home does too. Even a small change in mortgage rates can have a big impact on your purchasing power.

- If you put your search on hold when mortgage rates were higher, think about how much you could save now that rates are coming down.

Falling Mortgage Rates Are Bringing Buyers Back

If you’ve been hesitant to list your house because you’re worried no one’s buying, here’s your sign it may be time to talk with an agent.

After months of high rates keeping buyers on the sidelines, things are starting to shift. Rates are already coming down due to a number of economic factors. And yesterday the Federal Reserve cut the Federal Funds Rate for the first time since they began raising that rate in March 2022. And while they don’t control mortgage rates, this sets the stage for mortgage rates to fall even further than they already have – especially since more cuts from the Fed are expected into next year. And lower mortgage rates are bringing more buyers back into the market. Lisa Sturtevant, Chief Economist at Bright MLS, says:

“A drop in the cost of borrowing will help fuel more homebuyer demand . . . Falling rates will also bring more sellers into the market.”

The best part? You can take advantage of that renewed buyer interest.

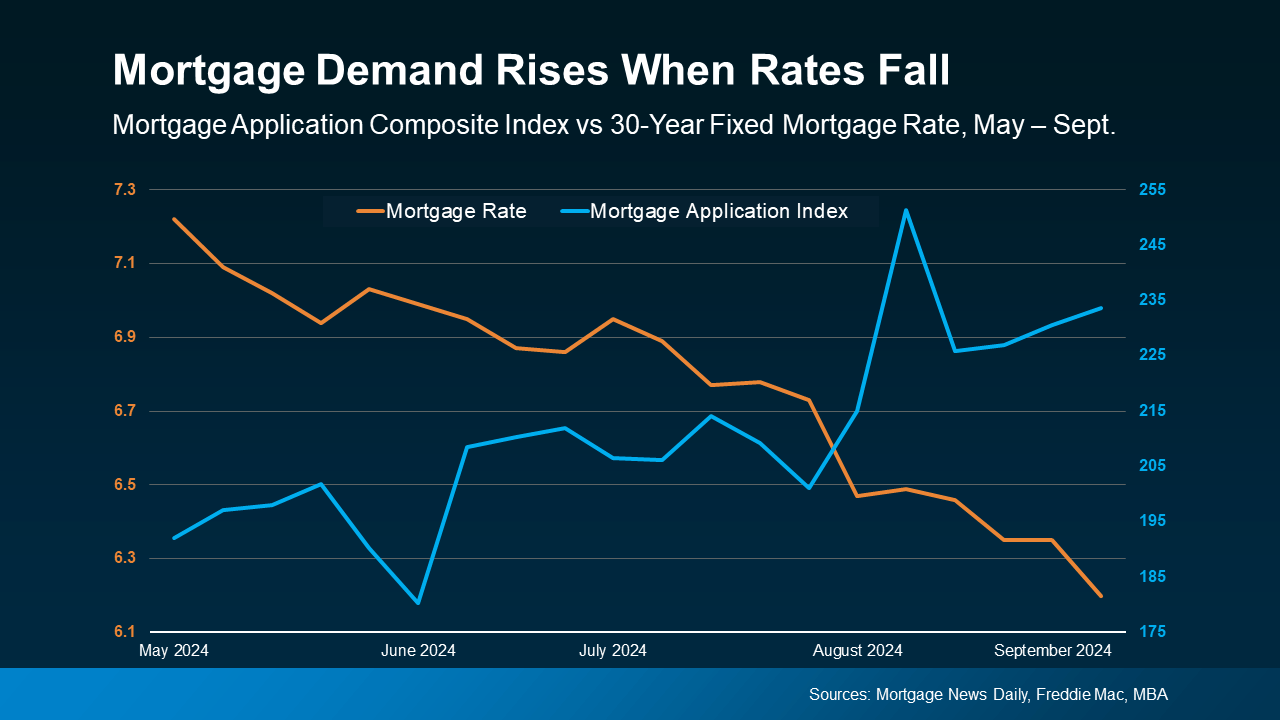

As Rates Fall, Buyer Activity Goes Up

The graph below illustrates the relationship between falling mortgage rates and rising buyer activity. The orange line represents the average 30-year fixed mortgage rate, while the blue line shows the Mortgage Bankers Association (MBA) Mortgage Application Index, which tracks the number of mortgage applications.

As you can see, as mortgage rates (orange) come down, the Mortgage Application Index (blue) rises, showing more people start to re-engage in the process (see graph below):

What This Means for You

What This Means for You

What This Means for You

What This Means for YouAccording to the National Association of Realtors (NAR), home sales increased in July, which was a welcome shift after four straight months of declines. If you’re a homeowner thinking about selling, this uptick in buyer activity works in your favor.

More buyers means more competition, which can lead to higher offers and shorter time on the market for your house. And, according to Edward Seiler, AVP of Housing Economics at the Mortgage Bankers Association (MBA), this trend is expected to continue:

“MBA is expecting that slower home-price appreciation, coupled with lower rates, will ease affordability constraints and lead to increased activity in the housing market.”

All in all, the market is becoming more accessible to a wider range of buyers, which could result in even more people looking to purchase a house like yours.

With more buyers entering the market, now’s the time to start getting your house ready to sell.

Bottom Line

The recent decline in mortgage rates is already driving more buyers into the market, and experts project this trend will continue. Work with a local real estate agent to take advantage of this increased buyer demand and get your house ready to sell.

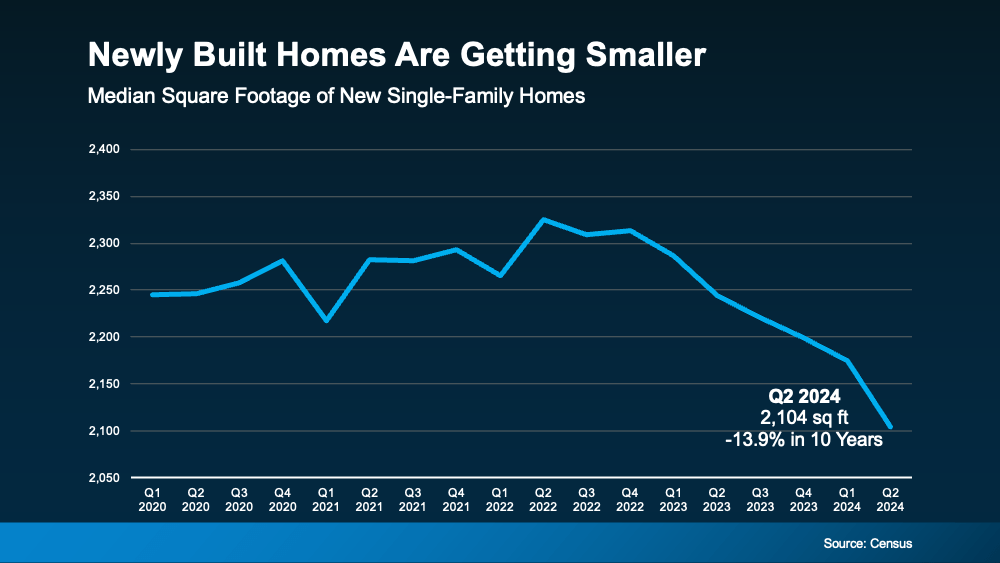

The Latest Builder Trend: Smaller, Less Expensive Homes

Even though affordability is improving, buying a home can still feel tough right now. But here’s some good news: builders are focusing their efforts on building smaller homes, and they’re offering key incentives to buyers. And both of these things can be a big help if you’re worried about finding a home that’s right for your budget.

Builders Are Building Smaller Homes

During the pandemic, homebuyers were looking for larger homes—and many could afford them. Builders responded to that demand and created bigger spaces to help people with things like working from home, setting up home gyms, and having extra rooms for virtual school.

Now, with affordability as tight as it is, builders are turning their focus to smaller single-family homes. Data from the Census shows how significant this trend toward smaller new homes has been over the last couple of years (see graph below):

But why would builders want to build smaller homes right now? At the end of the day, builders are going to focus on building homes that meet current market demand – because they want to build what they know will sell. And the number one thing homebuyers are looking for right now is better affordability. Since smaller homes typically come with smaller price tags, both buyers and builders have shifted their focus to homes with less square footage. The National Association of Home Builders (NAHB) reports:

But why would builders want to build smaller homes right now? At the end of the day, builders are going to focus on building homes that meet current market demand – because they want to build what they know will sell. And the number one thing homebuyers are looking for right now is better affordability. Since smaller homes typically come with smaller price tags, both buyers and builders have shifted their focus to homes with less square footage. The National Association of Home Builders (NAHB) reports:

“. . . home buyers are looking for homes around 2,070 square feet, compared to 2,260 20 years ago.”

And according to Orphe Divounguy, Senior Economist at Zillow:

“Not only are cash-strapped buyers continually seeking out lower-cost options, but developers are changing what type and size of home they’re producing to try and meet that need.”

How a Newly Built Home Can Help You Achieve Your Homebuying Goals

So, if you’re having a hard time finding something in your budget, it may be time to look at brand-new homes that have a smaller footprint. When you do, you may get a few other fringe benefits that can help on the affordability front – like price reductions or mortgage rate buy-downs.

According to the most recent data from Zonda, more than half of builders are offering incentives, some of which are mortgage rate buydowns. And those perks could help lower your future monthly housing payment too. John Burns, CEO of John Burns Research & Consulting, shares:

“The monthly payment matters more than anything else and builders have responded with smaller, more efficient homes.”

Not to mention, with new home construction, you’ll also get brand new everything, have fewer maintenance needs, and get some of the latest features available. That’s worth looking into, right?

Bottom Line

With builders focusing on smaller homes, you have more budget-friendly options when it matters most. If you’re thinking about buying a home soon, work with a local real estate agent to see what’s available where you want to live.

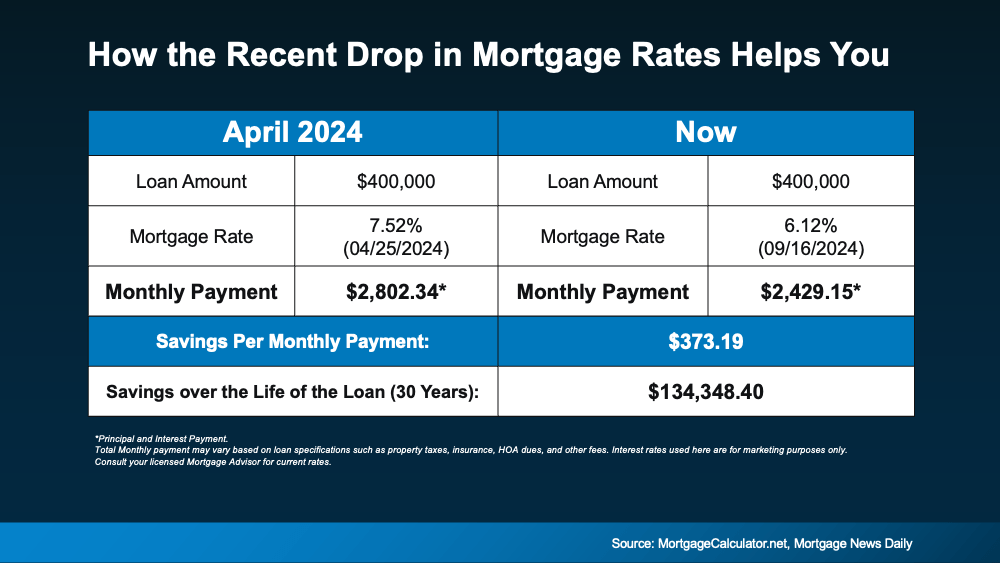

Mortgage Rates Drop to Lowest Level in over a Year and a Half

Mortgage rates have hit their lowest point in over a year and a half. And that’s big news if you’ve been sitting on the homebuying sidelines waiting for this moment.

Even a small decline in rates could help you get a better monthly payment than you would expect on your next home. And the drop that’s happened recently isn’t small. As Sam Khater, Chief Economist at Freddie Mac, says:

“Mortgage rates have fallen more than half a percent . . . and are at their lowest level since February 2023.”

But if you want to see it to really believe it, here’s how the math shakes out. Take a closer look at the impact on your monthly payment.

The chart below shows what a monthly payment (principal and interest) would look like on a $400K home loan if you purchased a house back in April (this year’s mortgage rate high), versus what it could look like if you buy a home now (see below):

Going from 7.5% just a few months ago to the low 6s has a big impact on your bottom line. In just a few months’ time, the anticipated monthly payment on a $400K loan has come down by over $370. That’s hundreds of dollars less per month.

Going from 7.5% just a few months ago to the low 6s has a big impact on your bottom line. In just a few months’ time, the anticipated monthly payment on a $400K loan has come down by over $370. That’s hundreds of dollars less per month.

Bottom Line

With the recent drop in mortgage rates, the purchasing power you have right now is better than it’s been in almost two years. Talk to a local real estate agent about your options and how you can make the most of this moment you’ve been waiting for.