Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

How Changing Mortgage Rates Can Affect You

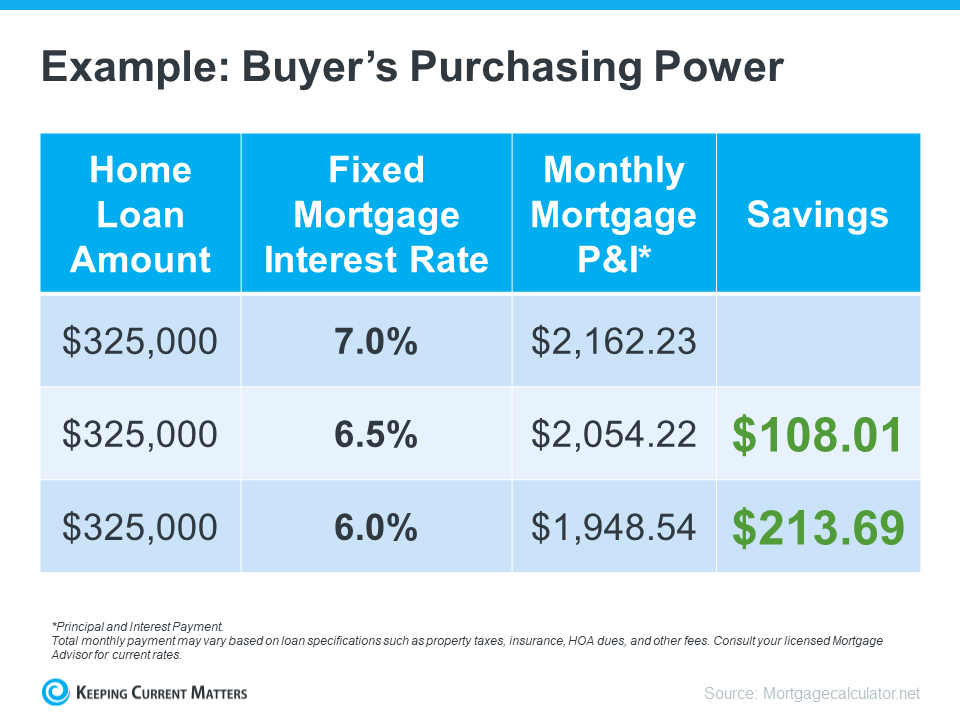

The 30-year fixed mortgage rate has been bouncing between 6% and 7% this year. If you’ve been on the fence about whether to buy a home or not, it’s helpful to know exactly how a 1%, or even a 0.5%, mortgage rate shift affects your purchasing power.

The chart below helps show the general relationship between mortgage rates and a typical monthly mortgage payment:

Even a 0.5% change can have a big impact on your monthly payment. And since rates have been moving between 6% and 7% for a while now, you can see how it impacts your purchasing power as rates go down.

What This Means for You

You may be tempted to put your homebuying plans on hold in hopes that rates will fall. But that can be risky. No one knows for sure where rates will go from here, and trying to time them for your benefit is tough. Lisa Sturtevant, Housing Economist at Bright MLS, explains:

“It is typically a fool’s errand for a homebuyer to try to time rates in this market . . . But volatility in mortgage rates right now can have a real impact on buyers’ monthly payments.”

That’s why it’s critical to lean on your expert real estate advisors to explore your mortgage options, understand what impacts mortgage rates, and plan your homebuying budget around today’s volatility. They’ll also be able to offer advice tailored to your specific situation and goals, so you have what you need to make an informed decision.

Bottom Line

Your ability to buy a home could be impacted by changing mortgage rates. If you’re thinking about making a move, partner with a trusted real estate agent and lender so you have a strong plan in place.

What Mortgage Rate Do You Need To Move?

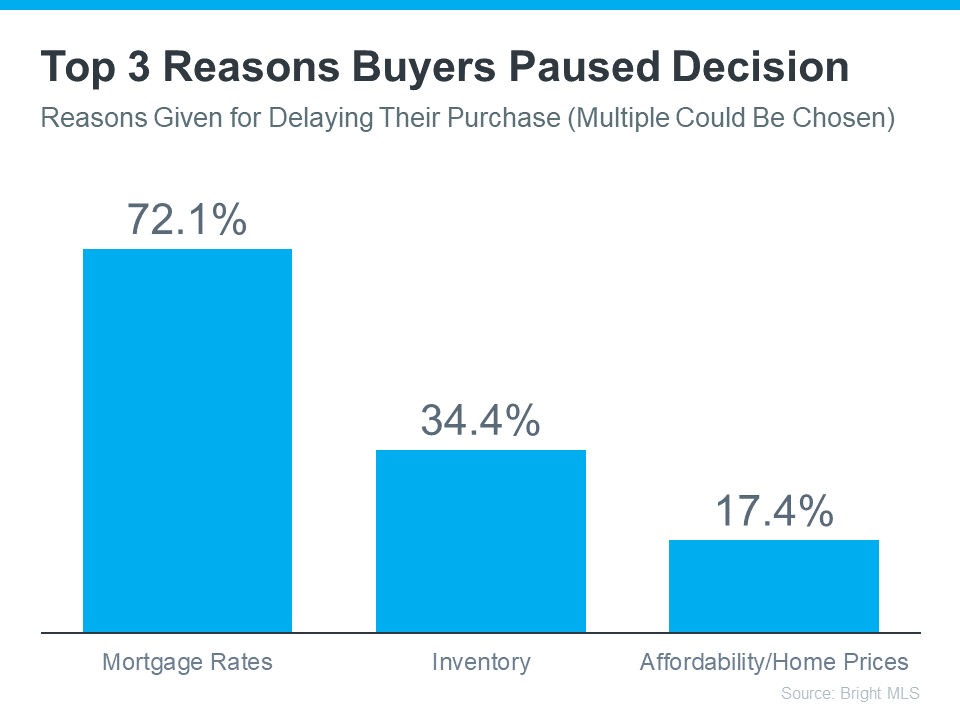

If you’ve been thinking about buying a home, mortgage rates are probably top of mind for you. They may even be why you’ve put your plans on hold for now. When rates climbed near 8% last year, some buyers found the numbers just didn’t make sense for their budget anymore. That may be the case for you too.

Data from Bright MLS shows the top reason buyers delayed their plans to move is due to high mortgage rates (see graph below):

David Childers, CEO at Keeping Current Matters, speaks to this statistic in the recent How’s The Market podcast:

“Three quarters of buyers said ‘we’re out’ due to mortgage rates. Here’s what I know going forward. That will change in 2024.”

That’s because mortgage rates have come down off their peak last October. And while there’s still day-to-day volatility in rates, the longer-term projections show rates should continue to drop this year, as long as inflation gets under control. Experts even say we could see rates below 6% by the end of 2024. And that threshold would be a gamechanger for a lot of buyers. As a recent article from Realtor.com says:

“Buying a home is still desired and sought after, but many people are looking for mortgage rates to come down in order to achieve it. Four out of 10 Americans looking to buy a home in the next 12 months would consider it possible if rates drop below 6%.”

While mortgage rates are nearly impossible to forecast, the optimism from the experts should give you insight into what’s ahead. If your plans were delayed, there’s light at the end of the tunnel again. That means it may be time to start thinking about your move. The best question you can ask yourself right now, is this:

What number do I want to see rates hit before I’m ready to move?

The exact percentage where you feel comfortable kicking off your search again is personal. Maybe it’s 6.5%. Maybe it’s 6.25%. Or maybe it’s once they drop below 6%.

Once you have that number in mind, here’s what you do. Connect with a local real estate professional. They’ll help you stay informed on what’s happening. And when rates hit your target, they’ll be the first to let you know.

Bottom Line

If you’ve put your plans to move on hold because of where mortgage rates are, think about the number you want to see rates hit that would make you ready to re-enter the market.

Once you have that number in mind, connect with a real estate professional so you have someone on your side to let you know when we get there.

Renting or Selling Your House: What’s the Best Move?

If you’re a homeowner ready to make a move, you may be thinking about using your current house as a short-term rental property instead of selling it. A short-term rental (STR) is typically offered as an alternative to a hotel, and they’re an investment that’s gained popularity in recent years.

While a short-term rental can be a tempting idea, you may find the reality of being responsible for one difficult to take on. Here are some of the challenges you could face if you rent out your house instead of selling it.

A Short-Term Rental Comes with Responsibilities

Successfully managing your house as a short-term rental takes a lot of time and effort. You’ll have to juggle tasks like dealing with reservations, organizing check-ins, and tackling cleaning, landscape, and maintenance duties. Any one of those can feel demanding, but all together it’s a lot to handle.

Short-term rentals experience high turnover rates, as new guests check in and out frequently. This home traffic can lead to increased wear and tear on your property—meaning you may need to make more frequent repairs or replace your furniture, fixtures, and appliances more often.

Think through your ability to make that level of commitment, especially if you plan to use a platform that advertises your rental listing. Most of them have specific requirements hosts must meet. An article from Bankrate explains:

“Managing a rental property can be time-consuming and challenging. Are you handy and able to make some repairs yourself? If not, do you have a network of affordable contractors you can reach out to in a pinch? Consider whether you want to take on the added responsibility of being a landlord, which means screening tenants and fielding issues, among other responsibilities, or paying for a third party to take care of things instead.”

There’s a lot to consider before taking the leap and converting your house into a short-term rental. If you aren’t ready for the work it takes, it could be wise to sell instead.

Short-Term Rental Regulations

As the short-term rental industry continues to grow, regulations have increased. Legal restrictions commonly include limits on the number of vacation rentals in a particular location. This is especially true in larger cities and tourist destinations where there may be concerns about overcrowding or housing shortages for permanent residents. Restrictions may also apply to the type of property that can be used for short-term rentals.

Many cities also require homeowners to obtain a license or permit before renting out their properties. Nick Del Pego, CEO at Deckard Technologies, explains:

“Renting short-term rentals is considered a business by most local governments, and owners must comply with specific workplace regulations and business licensing rules established in their local communities.”

It is important to thoroughly check whether short-term rentals are regulated or prohibited by the local government and your homeowners association (HOA) before even considering renting out your home.

Bottom Line

Converting your home into a short-term rental isn’t a decision you should make without doing your research. To decide if selling your house is a better alternative, talk with a local real estate agent today.

Renting or Selling Your House: What’s the Best Move?

If you’re a homeowner ready to make a move, you may be thinking about using your current house as a short-term rental property instead of selling it. A short-term rental (STR) is typically offered as an alternative to a hotel, and they’re an investment that’s gained popularity in recent years.

While a short-term rental can be a tempting idea, you may find the reality of being responsible for one difficult to take on. Here are some of the challenges you could face if you rent out your house instead of selling it.

A Short-Term Rental Comes with Responsibilities

Successfully managing your house as a short-term rental takes a lot of time and effort. You’ll have to juggle tasks like dealing with reservations, organizing check-ins, and tackling cleaning, landscape, and maintenance duties. Any one of those can feel demanding, but all together it’s a lot to handle.

Short-term rentals experience high turnover rates, as new guests check in and out frequently. This home traffic can lead to increased wear and tear on your property—meaning you may need to make more frequent repairs or replace your furniture, fixtures, and appliances more often.

Think through your ability to make that level of commitment, especially if you plan to use a platform that advertises your rental listing. Most of them have specific requirements hosts must meet. An article from Bankrate explains:

“Managing a rental property can be time-consuming and challenging. Are you handy and able to make some repairs yourself? If not, do you have a network of affordable contractors you can reach out to in a pinch? Consider whether you want to take on the added responsibility of being a landlord, which means screening tenants and fielding issues, among other responsibilities, or paying for a third party to take care of things instead.”

There’s a lot to consider before taking the leap and converting your house into a short-term rental. If you aren’t ready for the work it takes, it could be wise to sell instead.

Short-Term Rental Regulations

As the short-term rental industry continues to grow, regulations have increased. Legal restrictions commonly include limits on the number of vacation rentals in a particular location. This is especially true in larger cities and tourist destinations where there may be concerns about overcrowding or housing shortages for permanent residents. Restrictions may also apply to the type of property that can be used for short-term rentals.

Many cities also require homeowners to obtain a license or permit before renting out their properties. Nick Del Pego, CEO at Deckard Technologies, explains:

“Renting short-term rentals is considered a business by most local governments, and owners must comply with specific workplace regulations and business licensing rules established in their local communities.”

It is important to thoroughly check whether short-term rentals are regulated or prohibited by the local government and your homeowners association (HOA) before even considering renting out your home.

Bottom Line

Converting your home into a short-term rental isn’t a decision you should make without doing your research. To decide if selling your house is a better alternative, talk with a local real estate agent today.

The Truth About Down Payments (It’s Not What You Think)

Buying a home is exciting… until you start thinking about the down payment. That’s when the worry can set in.

“I’ll never save enough.”

“I need a small fortune just to get started.”

“I guess I’ll just rent forever.”

Sound familiar? You’re not alone. And you’re definitely not out of luck.

Here’s the thing: a lot of what you’ve heard about down payments just isn’t true. And once you know the facts, you might realize you’re a lot closer to owning a home than you think.

Let’s break it all down and bust some big down payment myths while we’re at it.

Myth 1: “I need to come up with a big down payment.”

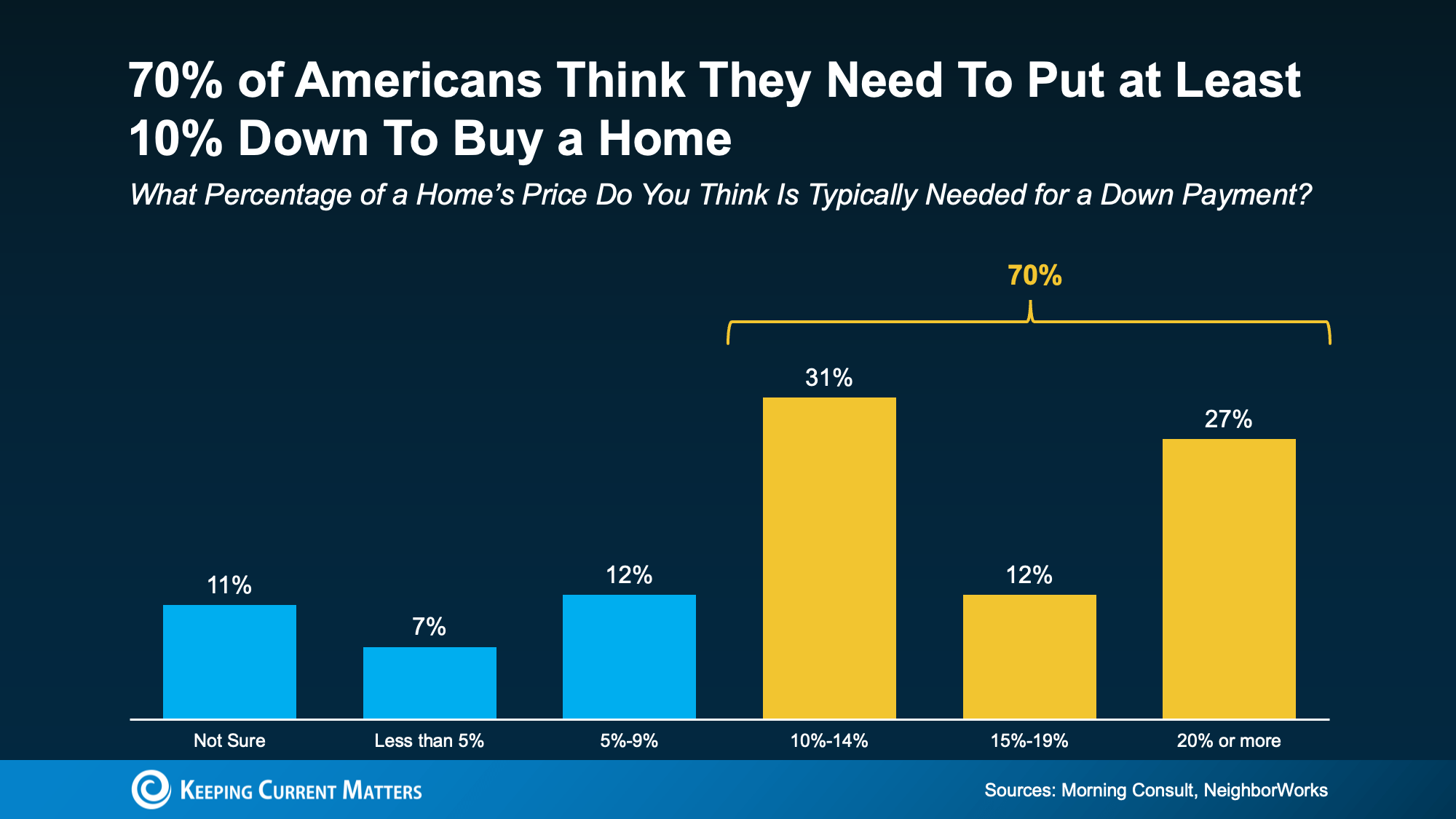

This one stops a lot of people in their tracks. A recent poll from Morning Consult and NeighborWorks shows 70% of Americans think they need to put at least 10% down to buy a home. And 11% aren’t sure what’s required at all (see graph below):

The truth? According to the National Association of Realtors (NAR), the typical down payment for first-time buyers has been between 6% and 9% since 2018. But there’s more to the story. If you qualify for an FHA loan, you may only need to put 3.5% down. And VA loans typically don’t require a down payment at all. So, there are options out there that can really make a difference for some buyers.

The truth? According to the National Association of Realtors (NAR), the typical down payment for first-time buyers has been between 6% and 9% since 2018. But there’s more to the story. If you qualify for an FHA loan, you may only need to put 3.5% down. And VA loans typically don’t require a down payment at all. So, there are options out there that can really make a difference for some buyers.

Myth 2: “It’ll take forever to save up for a down payment.”

Sure, saving can take time. But it may not have to be as long as you think. In many states, reaching your goal can happen faster than you might expect, especially when you know your budget and have a clear savings plan.

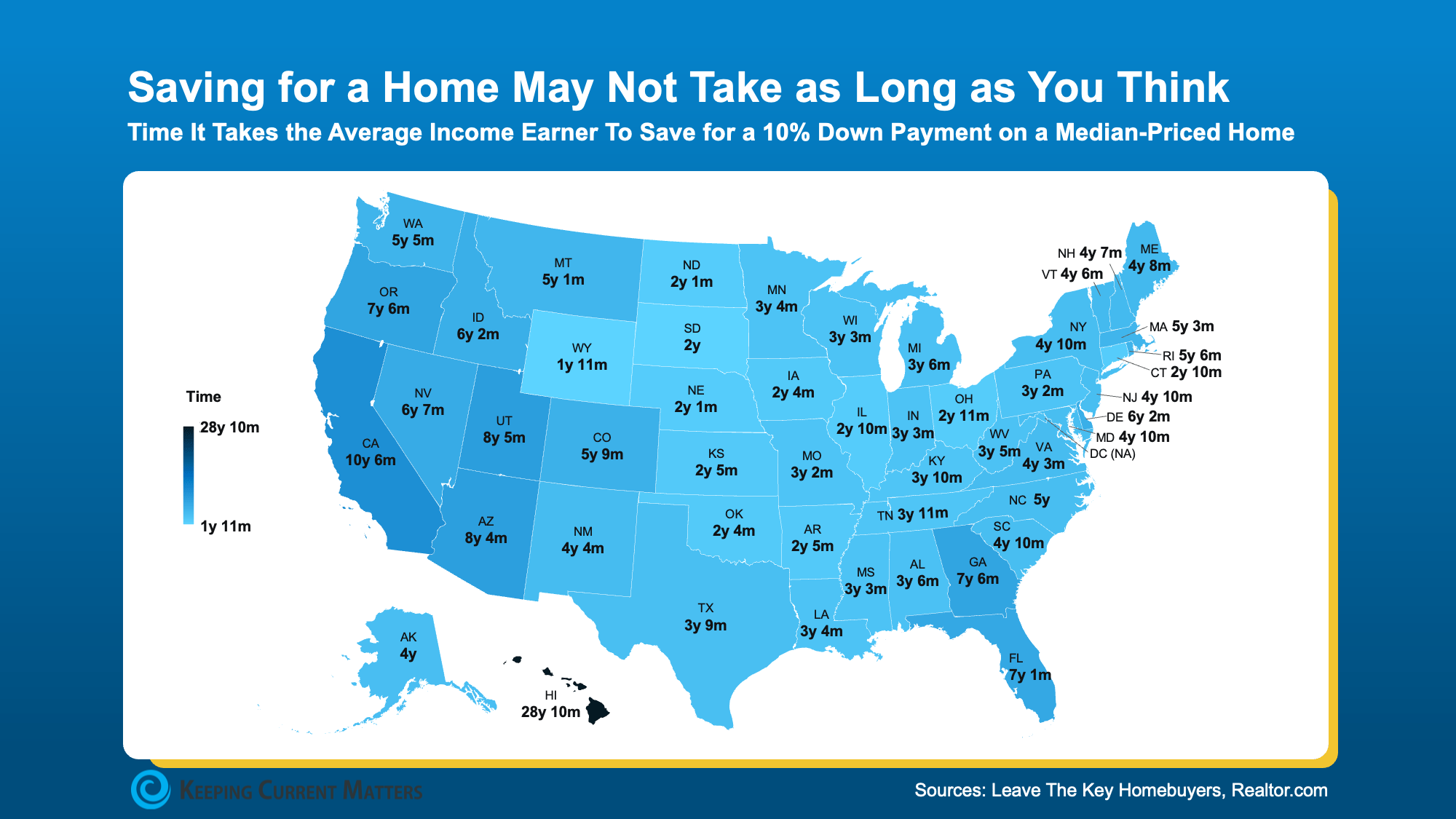

According to a new study, the amount of time varies depending on where you live. The map below shows, on average, how many years it takes to save up for a 10% down payment based on typical home values and income levels in each state (see map below):

But remember, in most cases you won’t even need a down payment as large as 10%. Plus, no matter how much money you end up putting down, it won’t all have to come out of your pocket. Here’s why.

But remember, in most cases you won’t even need a down payment as large as 10%. Plus, no matter how much money you end up putting down, it won’t all have to come out of your pocket. Here’s why.

Myth 3: “I have to do it all on my own.”

This is one of the biggest myths of all. The reality is, there are thousands of down payment assistance programs out there, and the same poll from Morning Consult and NeighborWorks shows 39% of people don’t even know about them. That means a lot of potential homebuyers could already be closer to homeownership – they just don’t realize it.

These assistance programs are designed to help people like you who are ready to own a home but just need a little support getting started. As Miki Adams, President at CBC Mortgage Agency, explains:

“With high interest rates and soaring home prices, down payment assistance is more essential than ever.”

Bottom Line

If you’ve been putting off buying a home because the down payment feels like too much to tackle, talk to a local real estate agent. You may not need as much as you think, and there are plenty of resources out there, so you don’t have to do it alone. You just need an expert to point you in the right direction.

If the down payment wasn’t the thing holding you back, would you be ready to start your home search?

The 3 Things You Risk by Pricing Too High

When selling your house, the price you choose isn’t just a number, it’s a strategy. And in today’s market, that strategy needs to be sharp.

The number of homes for sale is climbing. And that means buyers have more choices and can be more selective. If your price doesn’t line up with what else is out there, they’ll scroll right past it and go on to the next one.

Pricing right from the start is your best move – and a great agent can help make sure you do.

Overpricing Comes at a Cost

And more sellers are finding that out the hard way. They list their house based on how things were a year ago – or based on a neighbor’s sale that happened under completely different circumstances. Then, when their house doesn’t sell, they’re left with three tough choices:

- Drop the price: Cutting the price might help get more eyes on the house again, but it can also trigger red flags. Buyers may wonder what’s wrong with it. And that’s going to impact any offers you get after the price cut.

- Take it off the market: Some sellers give up on the idea of selling right now. The worst part about this is it means putting their future plans on the back burner. That dream of more space, downsizing, or relocating? On pause.

- Rent it out: Others go the landlord route, but managing tenants and navigating leases isn’t always the simple fallback it seems. Renting can work, but it’s often a lot more hassle than people expect.

None of those options were part of the original plan. And honestly, none of them are where you should end up if you wanted to sell. Here’s a look at how a local agent’s expertise can help you avoid these headaches. Let’s use price cuts as an example.

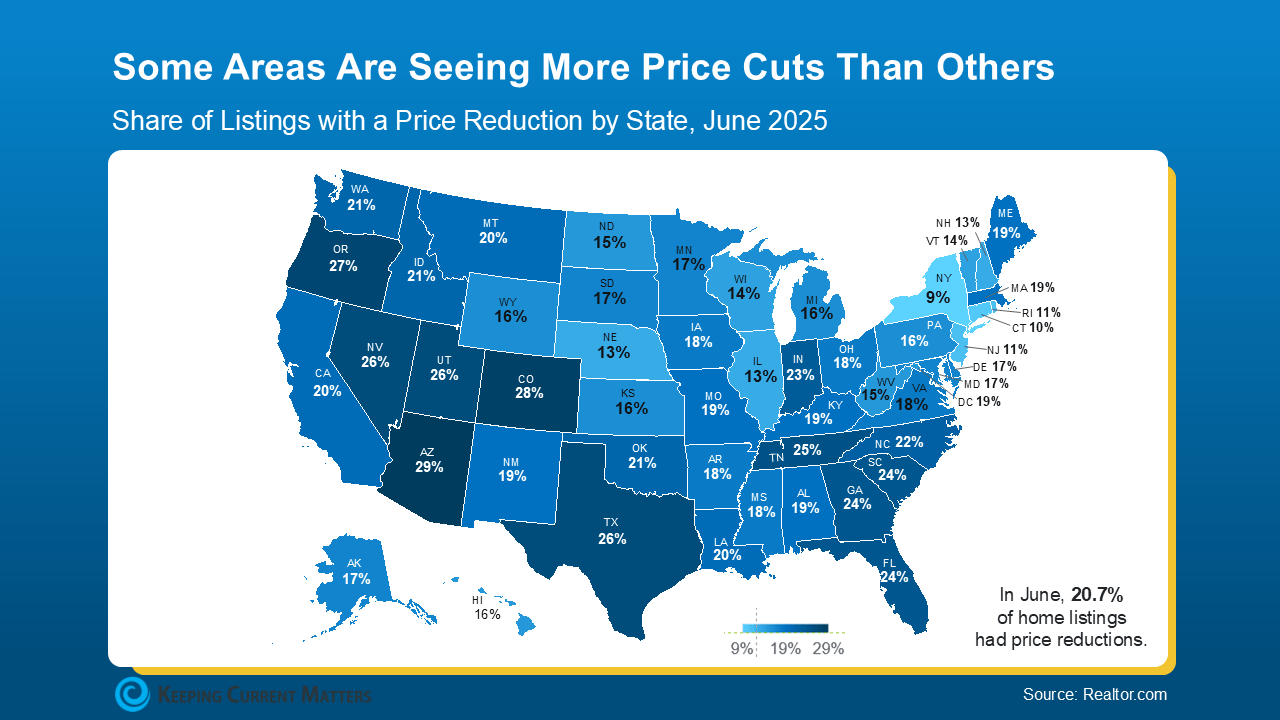

Where You Live Makes a Difference

While the number of price cuts is up nationally, data shows some parts of the country are seeing far more of them than others. It all comes down to how much inventory has grown in that area (see map below):

As Realtor.com explains:

As Realtor.com explains:

“Regionally, price reductions in June were significantly more common in the South and West (23% of listings) than they were in the Northeast (13% of listings), reflecting the inventory divergence across these regions.”

That means pricing isn’t one-size-fits-all. What’s happening nationally might not reflect what’s happening in your zip code, and that’s why you shouldn’t try to determine your list price on your own.

How a Great Agent Helps You Nail the Price

A skilled agent doesn’t just toss out a number. As Zillow says:

“Well-priced homes are more likely to sell quickly, but pricing your home to sell quickly and for maximum dollar requires strategy and knowledge of your local market. You need to have a clear-eyed view of your home in relation to the competition, and knowledge about whether you’re in a buyers or sellers market. It also helps to know what buyers in your area can afford.”

And that’s all knowledge your agent will have. They study your local market, compare recent sales, and factor in your goals and buyer behavior. Based on what’s happening where you live, sometimes the best play will be pricing right at current market value. Other times pricing a little lower actually will spark more offers and ultimately get you a better final sale price.

So don’t skimp on the strategy or on your agent. With their local market know-how, you’ll be able to sell quickly, even in a shifting market.

Bottom Line

Overpricing can lead to tough choices you never want to face. But with the right price, and the right guidance, you can skip the stress and sell with confidence. Connect with a local agent so you have a pricing strategy that works for today’s market and gets you where you want to go.